German central bank: ”Gold is the bedrock of stability for the international monetary system”

Jan Nieuwenhuijs

Gold Analyst

Central banks have changed their tone on gold

It was long believed in the gold space that Western central banks are against gold, but things have changed, for quite some years now. Instead of discouraging people from buying gold, or convincing them that gold is an irrelevant asset, many of these central banks are increasingly honest about the true properties of this monetary metal. Stating that gold is the ultimate store of value, that it preserves its purchasing power through time and is a global means of payment. Such statements, combined with actions that will be discussed below, reveal that more and more central banks are preparing for plan B.

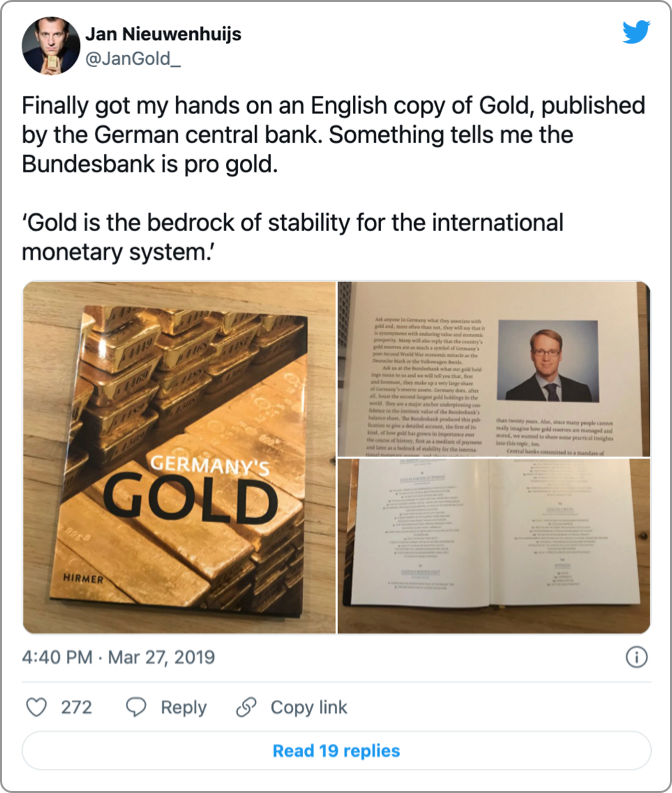

The Bundesbank (the German central bank) published a book last year named Germany's Gold. In the introduction, written by the President of the Bundesbank Jens Weidmann, the view of this bank leaves no room for interpretation. Weidmann writes (emphasis mine):

Ask anyone in Germany what they associate with gold and, more often than not, they will say that it is synonymous with enduring value and economic prosperity.

Ask us at the Bundesbank what our gold holdings mean for us and we will tell you that, first and foremost, they make up a very large share of Germany's reserve assets ... [and they] are a major anchor underpinning confidence in the intrinsic value of the Bundesbank's balance sheet.

The Bundesbank produced this publication to give a detailed account, the first of its kind, of how gold has grown in importance over the course of history, first as medium of payment, later as the bedrock of stability for the international monetary system.

Jens Weidmann, President of the Bundesbank

For Keynesians, these comments might read like the Bundesbank (BuBa) is a “goldbug”. Its remarks, however, are simply common sense. Gold has enduring value. The world over it is associated with economic prosperity. Every reserve currency in the world today is underpinned by vast gold reserves. Otherwise, monetary authorities wouldn't trust holding the respective currencies, next to holding their own gold reserves. Gold truly is the bedrock of stability for the international monetary system.

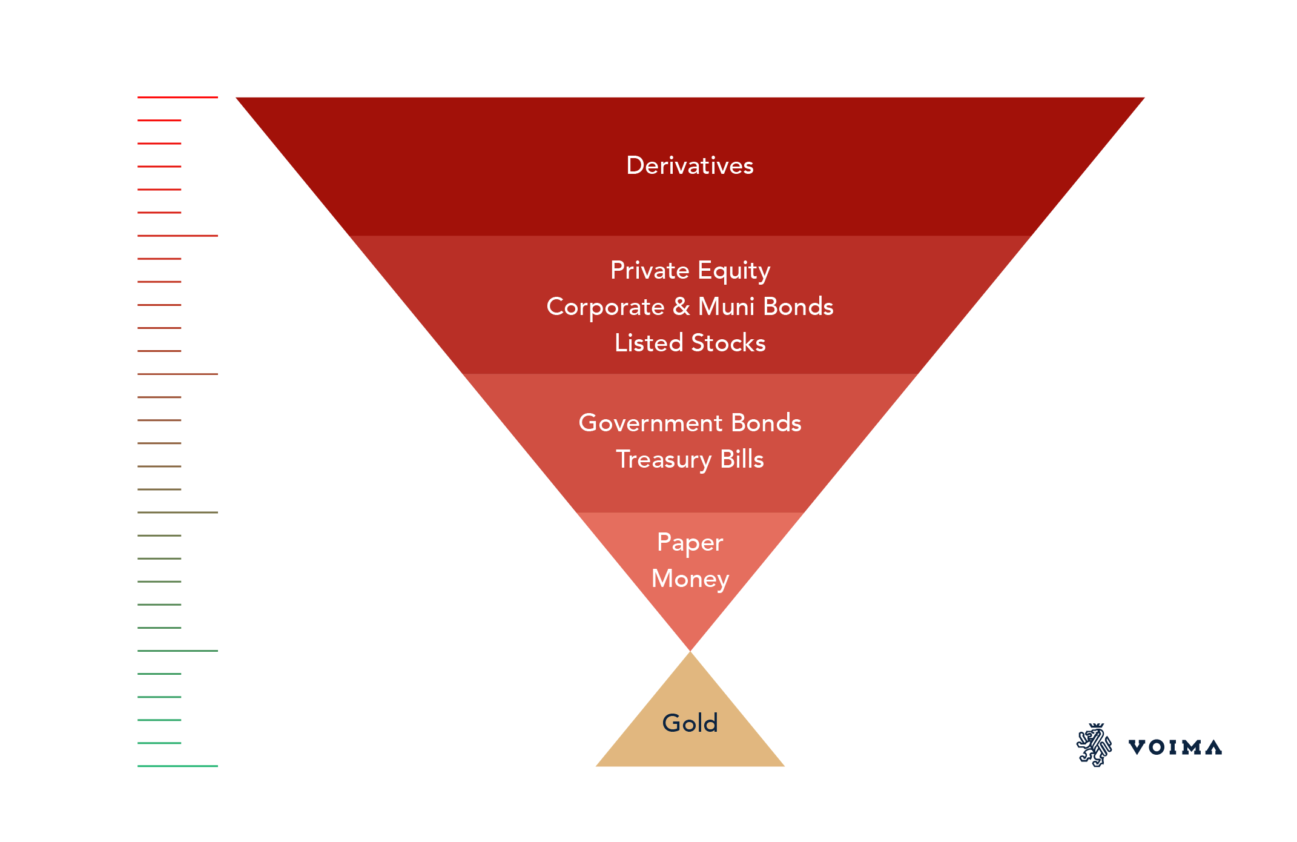

Central banks and Exter's pyramid

What springs to mind when reading Weidmann's statement is Exter's Inverse Pyramid. John Exter was an American economist that in the 1960s conceived an upended pyramid of financial assets. Underneath the pyramid is gold that forms the base of most reliable value; all asset classes within the pyramid on progressively higher levels involve more risk. Exter would sometimes refer to his model as the debt pyramid; hence, he positioned gold outside of it as it's the only asset that has no liability against it.

Tellingly, when Exter addressed the Economic Society of South Africa in Johannesburg on 16 November 1966, he said:

Gold is the hard core of our international monetary system.

John Exter

“Bedrock” (Weidmann) and “hard core” (Exter) are similar, and both point to gold's strength and what it can carry. An essential element of capitalism is investing—directly, indirectly, through bonds or equity—that involves risk. The higher the risk, the higher the return. The lower the risk, the lower the return. What falls outside of the investment realm has zero risk and no return, but provides the base that carries the debt system. This safe haven is gold, the only asset refuge that has no counterparty risk.

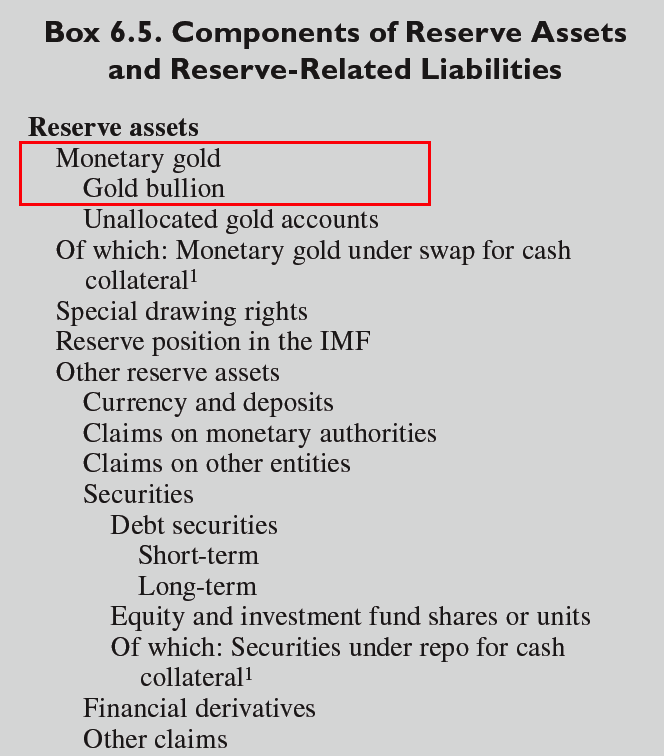

In the Balance of Payments and International Investment Position Manual (BPM6) drafted by the International Monetary Fund (IMF), we read:

Financial assets are economic assets that are financial instruments. Financial assets include financial claims and monetary gold held in the form of gold bullion … A financial claim is a financial instrument that has a counterpart liability. Gold bullion is not a claim and does not have a corresponding liability. It is treated as a financial asset, however, because of its special role as a means of financial exchange in international payments by monetary authorities and as a reserve asset held by monetary authorities.

IMF

The IMF considers all financial assets to have counterparty risk, except gold.

On page 112 of BPM6, the IMF lists all international reserve assets by descending order. Crowning the lineup is physical gold, followed by cash, debt securities, equity and finally derivatives. Nearly an exact copy of Exter's Pyramid.

Another appearance of the pyramid can be found on the website 1 of the Dutch central bank, De Nederlandsche Bank (DNB). Since April 2019, DNB's gold information page reads:

A bar of gold always retains its value, crisis or no crisis. This creates a sense of security.

Shares, bonds and other securities are not without risk, and prices can go down. But a bar of gold retains its value, even in times of crisis. That is why central banks, including DNB, have traditionally held considerable amounts of gold. Gold is the perfect piggy bank—it's the anchor of trust for the financial system. If the system collapses, the gold stock can serve as a basis to build it up again. Gold bolsters confidence in the stability of the central bank's balance sheet and creates a sense of security.

DNB

Exter's pyramid all over. Kindly note the similarity between DNB's and BuBa's comments on gold providing essential confidence in their balance sheets. It goes to show these two central banks have a long history of cooperating.

I tweeted about DNB's candid approach last April (a few months later, it went viral).

European central banks on gold

Let's continue with another quote, this time from the Bank of Finland (BOF):

Gold – The basis of a monetary system

Gold is called the eternal payment instrument and has been used as a medium of exchange for thousands of years. Gold is a genuinely global means of payment that has maintained its value throughout history.

BOF

One more, from the Banque de France (BDF):

Key facts

Gold is a highly sought-after precious metal, considered to be the ultimate store of value.

BDF

All central banks quoted agree gold preserves its purchasing power through time.

Preparing for Plan B

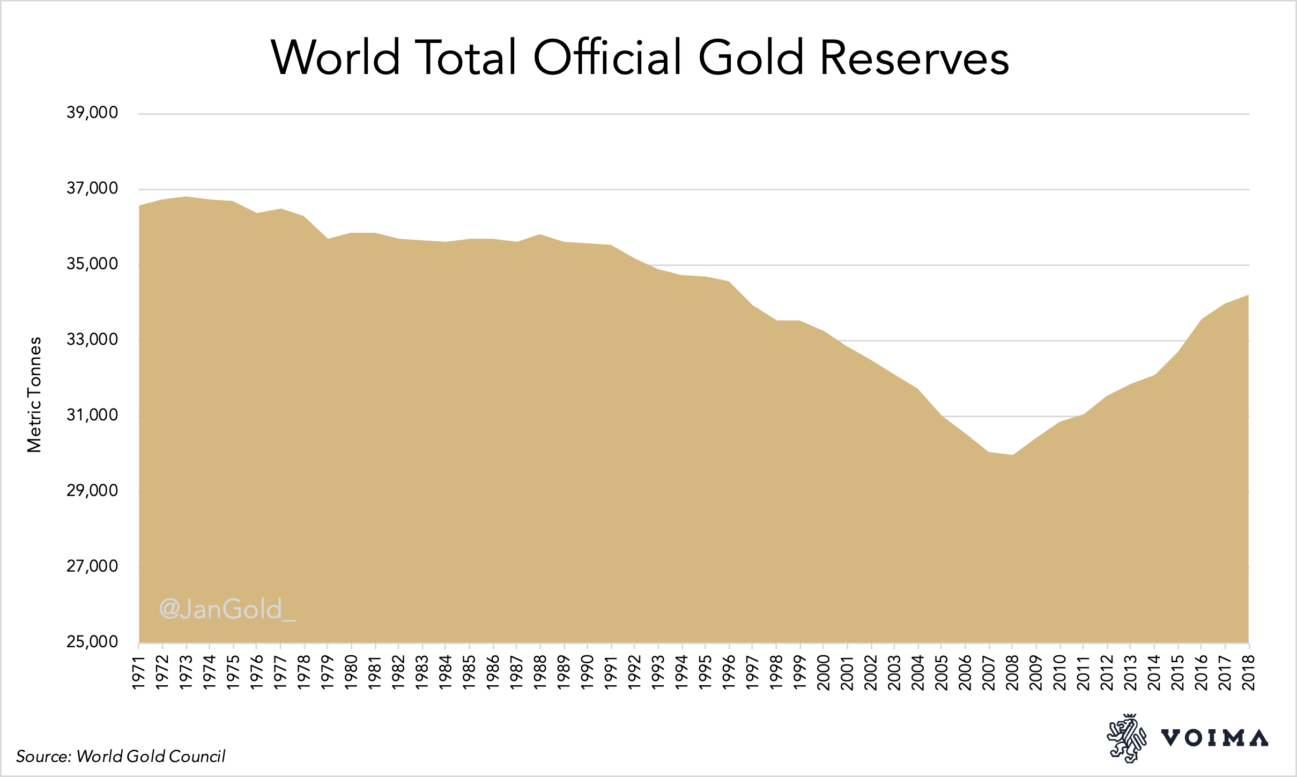

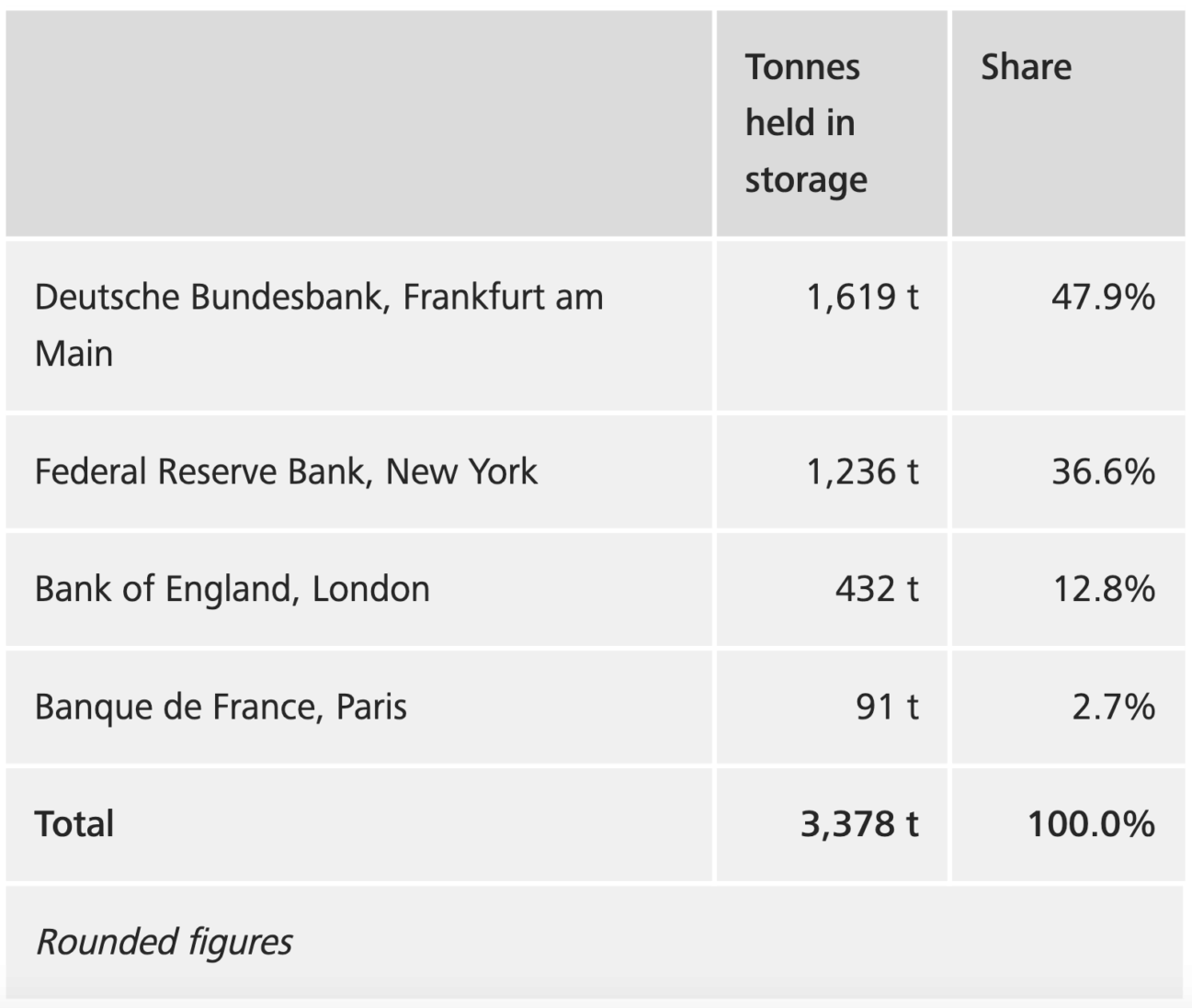

Next to strong statements by central banks, they're acting accordingly. Shortly after the Great Financial Crisis (GFC), central banks as a sector became net buyers and Germany, the Netherlands, Austria, Hungary and Turkey, among others, repatriated gold. Mainly from the Bank of England in London and the Federal Reserve Bank of New York.

According to BuBa, their repatriation scheme had three objectives: cost efficiency, security and liquidity. Cost efficiency is about the storage costs in every location. Security involves the safety of the vaults and where those vaults are. The current trend is to have a significant fraction of gold on home soil due to the geopolitical environment. Liquidity is about owning bars that adhere to prevailing industry standards and are located in liquid marketplaces such as London, i.e., to make payments in times of changes in the financial system. This latter aspect deserves special attention.

As we've seen, Western monetary authorities mention gold to be “the anchor of trust for the financial system”, “the bedrock of stability for the international monetary system” and “a genuinely global means of payment”. They're also saying that “if the system collapses, the gold stock can serve as a basis to build it up again”. One wonders if these entities are preparing for a new type of international gold standard. They see it as one possible outcome, as in recent years, several central banks have upgraded their gold reserves to current gold industry standards, also referred to as London Good Delivery.

Throughout history, bars of different purities were traded in wholesale markets. By 1954, every new bar accepted in the London Bullion Market—the centre of gold trade since the 18th century—was required to be at least 995 parts per thousand fine and weighing in between 350 and 430 fine troy ounces. Although not every old bar was promptly upgraded. Some remained as they were, in vaults in London and other places. These bars now trade at a discount, usually equal to the cost of upgrading and, if necessary, transporting them to London.

After the GFC many central banks were holding bars that were cast before 1954, which are currently not liquid in wholesale markets. In response, the French, Swedish and German central banks, that I know of, have upgraded their gold reserves to solve this liquidity issue.

From the BDF:

Since 2009, the BDF has been engaged in an ambitious programme to upgrade the quality of its gold reserves. The target is to ensure that all its bars comply with LBMA [London Bullion Market Association] standards so that they can be traded on an international market.

BDF

From the Swedish Riksbank:

To ensure that the Riksbank has the most liquid gold reserve possible, in 2017 the Riksbank upgraded the part of its gold reserve that did not meet the LGD [London Good Delivery] standard by replacing these bars with new gold bars that do meet the standard.

Riksbank

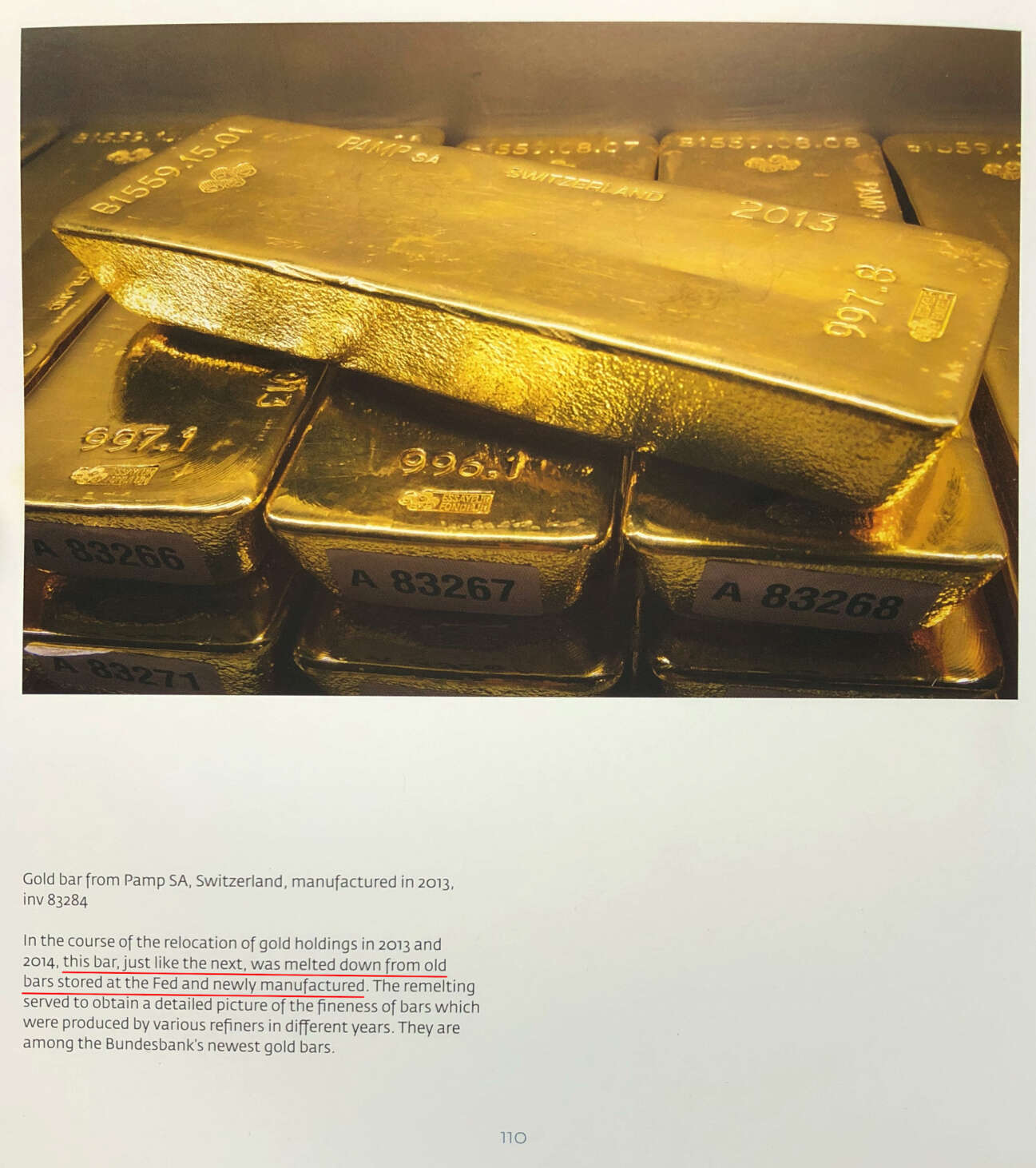

I don't have a quote from BuBa itself on their upgrade operation. However, connecting a few dots uncovers when and how they did it. BuBa released a bar list in 2015 disclosing all their gold to be 995 fine or higher. In the book Germany's Gold, a bar is displayed on page 110 with the subscription:

In the course of the relocation [repatriating] of gold holdings in 2013 and 2014, this bar … was melted down from old bars stored at the Fed and newly manufactured. The remelting served to obtain a detailed picture of the fineness of bars which were produced by various refiners in different years. They are among the Bundesbank's newest gold bars.

BuBa

While BuBa states this bar was melted for assaying purposes, in reality, it was part of making their entire stack at least 995 fine. One, because it doesn't require melting a whole bar for assay testing. Two, on 11 November 2017, the Financial Times published an article on how BuBa repatriated its gold. The article states:

[...] more than 4,400 bars transferred from New York were taken to Switzerland, where two smelters remoulded the bullion into bars that meet London Good Delivery standards for ease of handling.

Financial Times

Just like that one bar wasn't melted to “obtain a detailed picture of the fineness”, the 4,399 bars weren't melted “for ease of handling”. They were all refined for one reason: to meet London Good Delivery criteria and make Germany's gold reserves wholly liquid.

Conclusion

According to John Exter, when the debt pyramid has grown in excess and becomes unstable, bubbles burst. Investors, seeking safety, will run down the ladder until they find solid ground (the bedrock). This foundation is gold, which can't default or be arbitrarily devalued.

The GFC was caused by too much debt (a credit binge). When Lehman fell and the house of cards came crumbling down, the quickest solution authorities could think of, ironically, was more debt. We went from “extend and pretend” to “delay and pray”. Central bank intervention can be effective, for a while, until the underlying problem resurfaces with a vengeance. Presently the world is more in debt than before the GFC. The Institute of International Finance estimates global debt to GDP is now 320%.

When reading the mainstream media, one can be persuaded to think all central banks are willing to “print” money to infinity and lower interest rates as far as they can—or launch a variety of the same—pushing us further into the abyss. Some of them, though, aren't that ignorant and are actively preparing for when paper currencies are forced to be devalued by the weight of debt issued in said currencies.

There's one more development at a Western central bank I like to share. The BDF—whose vaults were a vibrant part of the global gold market during the classical gold standard—has not only upgraded its metal but also enhanced its entire vaulting infrastructure since the GFC. From the BDF:

Since the 2008 financial crisis, there has been renewed interest in gold from reserve managers.

As well as upgrading its stock, the Banque de France is taking various other steps to ensure it meets LBMA criteria [these standards apply for trading across the globe] … The renovation of the historical vaults housing the gold reserves has nearly been completed: the floor will be able to support heavy forklift trucks, and intermediary shelves have been inserted between the existing shelves to ensure the gold is only stacked five bars high, making handling easier. Other storage facilities will be available soon: either strong rooms for storing bare bars on shelves or large vaults to store sealed pallets, facilitate handling, transportation and auditing. By the end of the year, a new IT system will be in place to improve our ability to respond to market operation needs and other custody services.

BDF

So, after the GFC, not only have Western central banks changed the way they talk about gold—that is, they have become more honest regarding gold's function as a safe haven—but, as a sector, central banks have also become net buyers. Many central banks have redistributed their gold, carefully considering all possible future risks and developments. A few central banks have upgraded their gold to current industry standards to be able to trade frictionless in international markets. One central bank, BDF, has even enhanced its entire vaulting infrastructure. And this is just based upon publicly available information.

We're all too familiar with central banks in the East openly buying gold, stimulating citizens to buy gold, setting up new gold exchanges and de-dollarising. In the West, these subjects are more sensitive for political reasons. As a result, since the GFC, Western central banks gently started moving towards gold, not to cause any shocks in the market. In 2015, I called this “the slow development towards gold”, and it's continuing still.

It's beyond the scope of this article to discuss every probable international monetary development and attribute a percentage chance to each of them. I think it's clear though, that many central banks are preparing for gold to play a resolving and pivotal role in future global finance. Why else buy, redistribute and upgrade gold, next to enhance trading facilities, increase transparency and then advertise gold's financial features? Keep in mind what Pericles said around 500 BC: “The key is not to predict the future but to prepare for it.”

Currently, Exter's Pyramid has grown too big and is unstable. The moment the pyramid falls “gold will do its job”. History teaches us gold protects its owners through all types of weather, and central banks know this. Ever wondered why virtually every central bank owns gold? Because gold is physical. Immutable, yet divisible. Independent and without counterparty risk. It is the ultimate store of value—as it retains its purchasing power through time—and works as an eternal payment instrument.

The views expressed on this post are those of the author and do not necessarily reflect the official views or position of Voima.

You are allowed to copy our content, in whole or in part, provided that you give Voima proper credit and include the appropriate URL. The name Voima and a link to the original post must be included in your introduction. All other rights are reserved. Voima reserves the right to withdraw the permission to copy content for any or all websites at any time.

Nothing written in Voima's blog or website constitutes investment, legal, tax or other advice. It should not be used as the basis for any investment decision which a reader thereof may be considering. The purpose of Voima's blog is to provide insightful and educational commentary and is not intended to constitute an offer, solicitation or invitation for investing in or trading gold.