Why gold?

The benefits of gold ownership:

- Real asset class diversification

- Greater risk-adjusted returns, as proven by data

- Deep liquidity—gold exchanges roughly €120B per day

- Gold is the only asset class that does not carry a counterparty risk

- The most stable currency historically, with a broad owner base

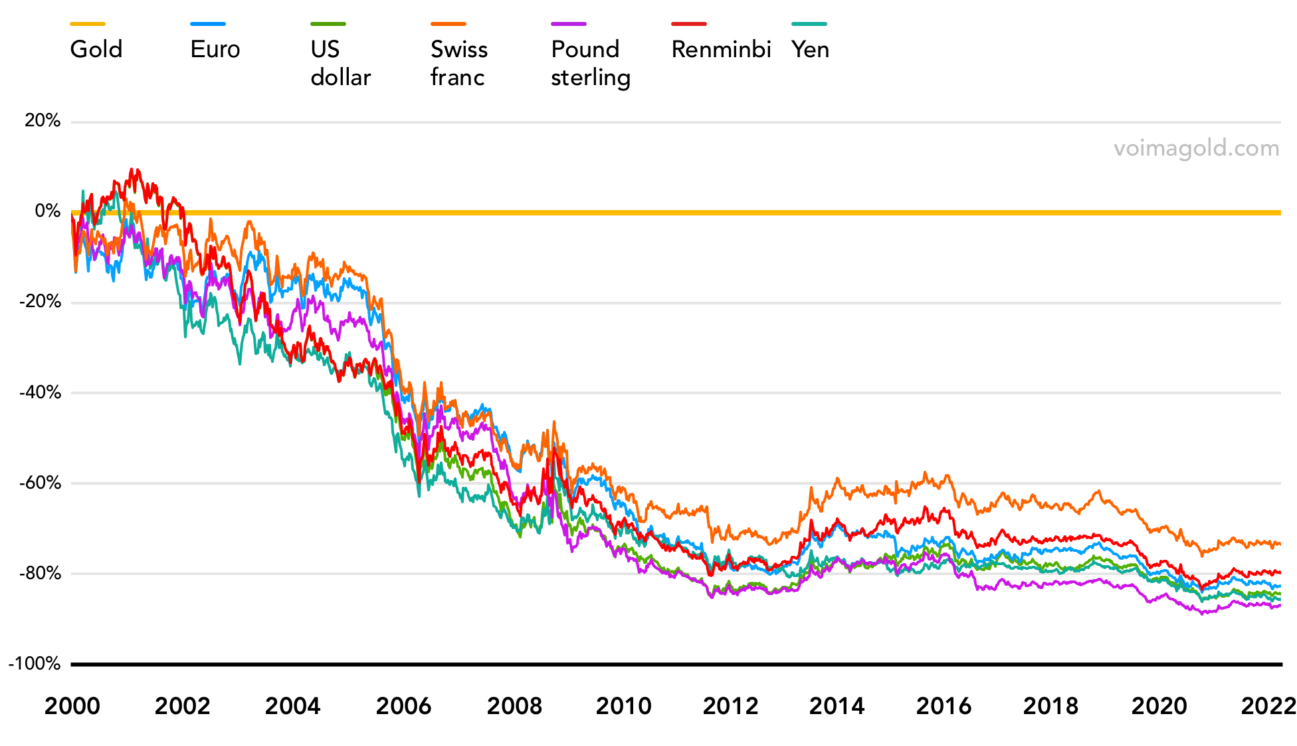

Gold and other currencies

Financial instruments such as stocks, bonds and apartments carry a risk of future cash flows, and along with this risk come the calculable returns.

Gold, on the other hand, should not be compared to such investments. Even though gold is a physical asset, it is held in central banks' FX reserves alongside other currencies, and it is traded internationally on FX markets. Just like other currencies, gold does not yield anything and thus there is no associated risk of future cash flows.

However, in contrast to other currencies, gold does not have a central bank that could create it out of nothing. Thus gold is the only asset that truly does not carry a counterparty risk.

Gold in portfolio

According to various comprehensive studies (Bank for International Settlements (BIS), World Gold Council), gold allocation improves the risk-adjusted returns of an institutional portfolio. In other words, it decreases volatility and increases the absolute returns.

Among other things, gold's deep liquidity and its data-backed track record in the improvement of the risk-adjusted returns of institutional portfolios make it a unique asset class. Gold is also a physical metal and not, for example, a debt instrument or a security. Independence and good financial ratios make gold an excellent instrument for diversification.

The aforementioned factors and gold's role as a historical store of value are also why central banks always have gold on their balance sheets. In addition, gold offers unparalleled protection and liquidity against systematic risks.

| Index / Asset | Annualised return | Annualised return in gold | Volatility average (12 months) | Correlation with gold (EUR) |

|---|---|---|---|---|

| Gold (EUR) | 8.78% | 0.00% | 15.36% | 1.00 |

| OMXHPI (EUR) | −0.46% | −8.49% | 24.40% | 0.08 |

| OMXHGI (EUR) | 3.70% | −4.67% | 24.37% | 0.67 |

| MSCI EM (EUR) | 3.87% | −4.51% | 18.82% | 0.86 |

| US 10-Year Treasuries (USD) | 1.49% | −7.00% | 5.71% | 0.91 |

| S&P 500 (USD) | 6.02% | −2.84% | 18.15% | 0.75 |

Institutional gold allocations

From Bridgewater Associates to the Dutch pension fund DSM, major investors tend to have a long-term allocation in gold. We have gathered a list of some of the major institutional investors that have allocated funds into gold.

| Organisation | Allocation | Source | Source date |

|---|---|---|---|

| Bridgewater Associates LP | 1.30 million GLD / SPDR Gold Trust (ETF) shares (227.5 million USD) 2.36 million IAU / iShares Gold Trust shares (84.2 million USD) |

Link | 10 January 2023 |

| Teacher Retirement System of Texas | 0.28 million GLD / SPDR Gold Trust shares (48.6 million USD) 2 million IAUM / iShares Gold Trust Micro shares (37.5 million USD) |

Link | 10 January 2023 |

| The Future Fund (Australia) | 200 million AUD | Link | 19 December 2022 |

| CPEV (Swiss pension fund) | Estimate: 2% | Q3 2022 quarterly report: Link Investment guidelines: Link News item: Link |

30 September 2022 |

| Koninklijke DSM N.V. (Dutch pension fund) | 386 million EUR | Link | 12 May 2021 |

Investment returns measured in gold

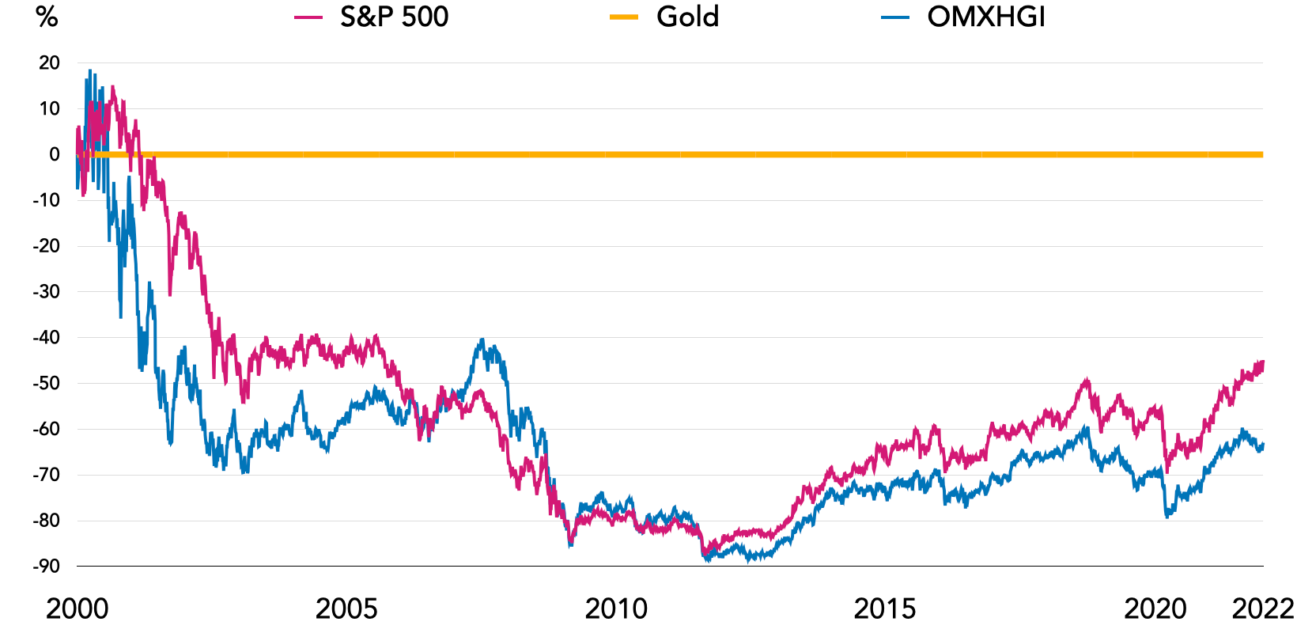

Weak national currencies such as the Turkish lira and the Argentine peso continuously lose purchasing power when measured in strong national currencies such as the euro or the dollar. What is often overlooked is that even these so-called strong national currencies lose purchasing power when measured in gold. This impacts the investment returns of assets denominated in euros and dollars. For an investor, looking at real returns means a lot more than looking at nominal returns. It simply does not make sense to measure returns with a yardstick that keeps on shortening.

When measuring the real returns in gold from the beginning of 2000 to the end of 2021, it turns out that none of the major asset classes had positive returns, as can be seen in the table above. This means that the investors who invested in stocks and bonds during this period have carried all the risks associated with these asset classes in their portfolio, but they still lost money compared to if they would have just held their purchasing power in gold for 21 years.

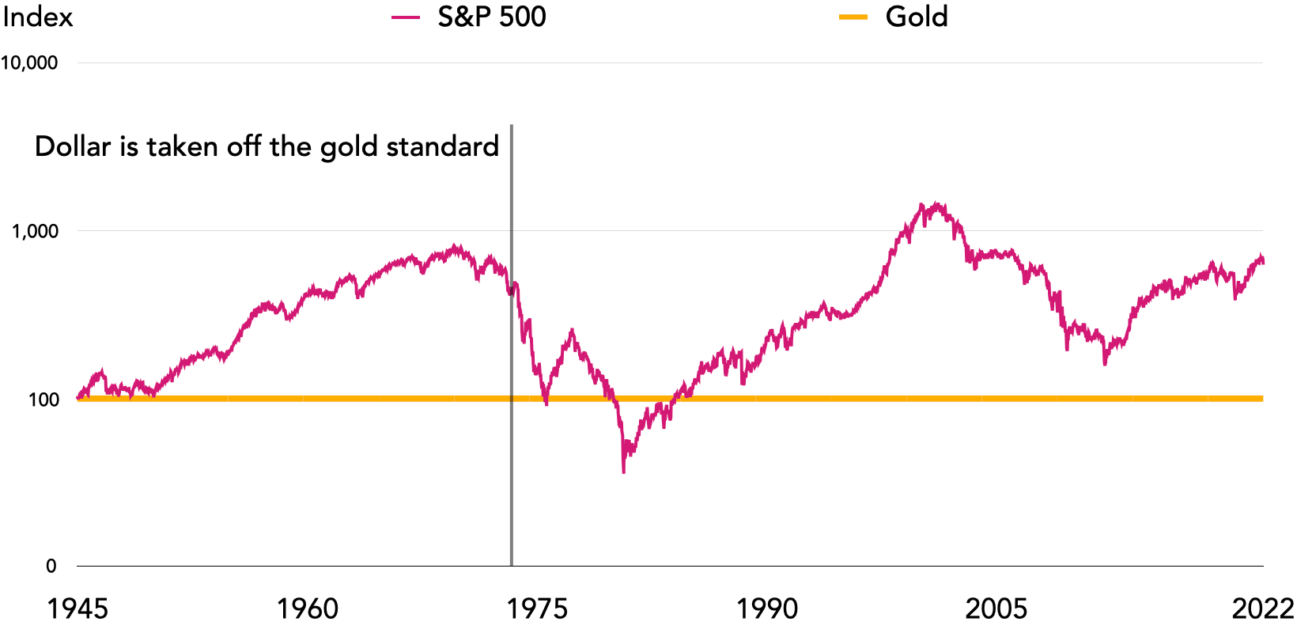

During the 1970s—a period in recent history known for high inflation and low growth, or stagflation—the S&P 500 index gained 17%, moving from 92 points to 108. However, this is the return measured in US dollars, whose value was decimated due to rampant inflation in the 1970s. When measured in gold, the S&P 500 lost 92% of its value during the high inflationary years of the 1970s.

As a matter of fact, at the end of 2021, the US benchmark equity index (S&P 500) was at the same level as it was in 1965 when measured in gold.

There is only one way to own gold

Large institutions and central banks own physical gold directly. This is contrasted with gold ETFs or gold futures, in which the gold is embedded in a complex structure of ownership. Direct ownership allows investors to reap all the benefits of owning gold and protect themselves against systematic risks.

A gold ETF is a share in a fund, whose holder in reality owns shares or zero-coupon perpetual bonds issued by the fund. Gold futures are derivative contracts. Both ETFs and futures are essentially IOUs, which involve a risk that the counterparty cannot meet their liabilities. In the worst case scenario, for example, if the ETF's custodian has to undergo debt restructuring, the gold might be used to pay off the custodian's debts.

Because one of the most significant advantages of gold over other asset classes is the lack of counterparty risk and the protection against a systematic risk, gold ownership should be as direct as possible.

An extract from Xetra-Gold® ETF's brochure

Xetra-Gold® investors only acquire the rights securitised in the notes. Investors do not acquire ownership / beneficial ownership or a lien to the gold held in custody in physical form on the issuer's behalf or to the issuer's rights on the unallocated weight account.

An extract from the prospectus of SPDR® Gold Trust

Although Shares are listed for trading on NYSE Arca, it cannot be assumed that an active trading market for the Shares will be maintained. If an investor needs to sell Shares at a time when no active market for Shares exists, or there is a halt in trading of securities generally or of the Shares, this will most likely adversely affect the price the investor receives for the Shares (assuming the investor is able to sell them).

Gold-backed euro bond

Voima also offers an interest product for professional investors, called Gold-backed euro bond.

Voima's subsidiary Voima Securities Oy (business ID: 3182353-6) funds the credit that Voima's Customers can take against their gold. The credit is financed by Gold-backed euro bond—a safe interest-bearing instrument for professional investors. The product pays competitive interest and is backed by real security.

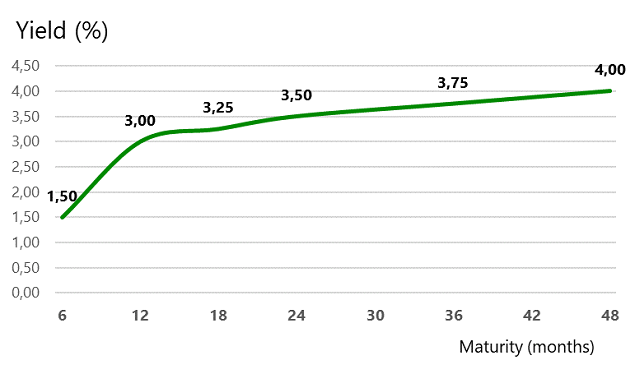

The gold on a Customer's Voima Account serves as collateral, and Voima Securities Oy's funds are used only to finance gold-backed credit, which makes the company's business clear and simple. If necessary, the collateralised gold will be sold, so that the credit is always fully backed. The high liquidity of gold and the markets that are active round the clock make gold excellent collateral that is easy to realise when necessary. The maturities range from three (3) months to forty-eight (48) months.

Feel free to contact Voima, if you are interested in Gold-backed euro bond.

Who qualifies?

Voima offers bespoke services to institutional Customers. The services are available globally.

Institutional Customers can be any of the following:

- Asset management and investment companies

- Holding and operating companies

- Foundations

- Governments and sovereign funds

- Municipalities

- Family offices

- Other organisations

Likewise, high-net-worth individuals (HNWIs) are also welcome to use the same services that are offered to institutional Customers.

Voima's institutional services

Voima Account affords easy management of assets.

Gain deep liquidity

- Voima Account offers institution-level liquidity and fast transaction settlements for gold

- Through Voima, the Customers can access the deep liquidity of international gold markets

Exchange euros and gold

- Buy and sell in real time

- Set up a recurring purchase or selling program for time diversification

Store gold safely in Finland

- Full insurance by Lloyd’s of London

- Audits by Bureau Veritas

Deposit gold to your Voima Account

- Gold transfers from other vaults can be arranged

- Loco London gold transfer and position conversions for Voima Account

Get custom reporting

- Reporting based on your needs

- Direct reporting to third parties on demand

Receive personalised service

- Voima's Vice President of Institutional Sales arranges any of these services for the institutional Customers

Converting existing positions for Voima Account

Even though ETF or futures positions do not grant gold ownership, many positions can be converted into physical gold through EFP (Exchange for Physical) and swap transactions. Voima has the capability to convert the following positions for the Customer's Voima Account:

- ETF or ETC instruments (XetraGold®, SPDR Gold Share, iShares Gold Trust)

- Gold futures (COMEX, LME)

- XAU gold accounts (Loco London, Loco Zürich)

Through its logistics network, Voima has the capability to transport bullion from other vaults to the company's own vault in Finland. The logistics are organised in cooperation with Brinks, Loomis and Nokas.

Feel free to contact Voima, if your portfolio has any other positions you would be interested in converting or transferring.

Reporting

Voima offers flexible and customised reporting for its institutional Customers. Whether you need daily valuations or semiannual reporting, Voima reports to you exactly as often and the way you require. If needed, Voima can also report directly to third parties.

Interested?

If you wish to become an institutional Customer or want to learn more about the relevant services, feel free to contact Henrik, our Vice President of Institutional Sales:

In case Henrik is temporarily unavailable, please get in touch with Voima's Customer care:

You may like these

2026-02-22

Voima Weekly #28 - The Age of Unlimited Money

Unlimited money supply, purchasing power, a metallic anchor, and balance sheet sustainability.

2026-02-08

Voima Weekly #26 - When Systems Buy Time

System erosion, production, debt, income transfers, and the EU structure.

2026-01-25

Voima Weekly #24 – Terms & Conditions

USA vs Europe: governance structure, debt, taxation, and the direction of the monetary system.