Gold in crises part 1: German hyperinflation

Lasse Lindholm

Community Manager

Table of contents

Introduction

This article series discusses how four of the most common assets have performed in four crises of recent history. The aim of the article series is to provide a background for the crises and give the reader an opportunity to protect their wealth today by using historical data.

The assets under review have been picked based on how common they are, namely stocks, bonds, housing and gold. For example forests and art have been left out, since they are not as relevant to common investors as the other assets: forests require a lot of maintenance, and art-as-investment usually has to do with very valuable, unique works. Art is also not valuated on the markets, but artworks are unique, which means that the unique characteristics of a work of art affect its value.

Apart from part 4, the reviewed assets are all local, meaning that for example in the case of Germany, we will only cover German investments.

The article series will discuss the following crises:

- German hyperinflation

- Great Depression (1930s)

- Stagflation in the 1970s

- War

The subjects under discussion involve essential factors in great economic crises, and all of them have taken place in a modern, developed economy.

This article deals with the German hyperinflation.

Inflation

First, we will take a general look at inflation and hyperinflation, and after that we will see which factors led to the depreciation of the German Papiermark and the resulting hyperinflation in 1923. Finally, we will examine how the assets performed in this hyperinflationary environment.

What is inflation and hyperinflation?

Inflation means the decrease of purchasing power or an increase in the prices of consumer products and services. Inflation levels are traditionally measured with consumer price indices that track the price development of particular consumer products. For example, in August 2022, the eurozone CPI had risen 9.1% compared to August 2021, meaning that the eurozone inflation was 9.1%.1

The fundamental cause of inflation is that central banks create more money into circulation. If central banks want to control inflation, they strive to decrease the amount of lent money in circulation. This is attempted by raising the key interest rate: when the key interest rate is raised, common banks hike their interest rates as well, which makes loans less appealing—this in turn is expected to curb consumption and thus inflation. The interest rate levels generally tend to rise during inflation, and the higher the expected inflation, the more the rates are expected to increase.

Interest rate hikes also have the effect that less loans are taken for investments, and thus there are generally less investments. This way, the prospects for economic growth weaken, since companies cannot develop their operations as effectively. As the growth prospects weaken, so does the companies' ability to hire new employees, which makes the employment situation more difficult. A prolonged inflationary period can thus at worst lead to mass unemployment.

According to the general interpretation, hyperinflation refers to a situation where the purchasing power of a currency is weakening at a monthly rate of 50% or the prices of consumer products rise 50% or more in a month.2 Throughout history, many currencies have been ravaged by hyperinflation, for example the Soviet ruble, Greek drachma, Hungarian pengő and the Yugoslav dinar. These days, for instance, the Turkish lira is undergoing hyperinflation.

German hyperinflation 1921–1923

A prolonged period of inflation preceded the German hyperinflation from 1914 to 1921. In 1914, Germany was preparing for World War I, and in order to provide the finances for this, Germany delinked the German mark from the gold standard. Because the German mark no longer corresponded to a particular amount of physical gold and thus was not tied to the amount of gold owned by the German state, they could print as much money as they wanted. The so-called Papiermark or “paper mark” became the sole currency in circulation.3 The currency change was followed by the issuing of new wartime bonds and debt instruments in order to finance the war. The new money ended up funneling into war equipment, and less so to the goods required by the civilians.4

The demand for the civilian goods exceeded the supply by far, since there simply were not enough goods available. As a result, the prices of consumer goods skyrocketed. In 1921, the price of rye bread had risen 13-fold and that of beef 17-fold compared to 1913. In the same period, milk, pork and potatoes cost 23–28 more, whereas butter ended up being 33 times more expensive.5

After the war in 1923, Germany also supported the passive resistance of the German workers in the industrial area of Ruhr, which was occupied by the Allied forces. In order to persuade the German workers not to cooperate with the Allied troops, the German state reimbursed the German people living in the Ruhr area their daily wages in return for the resistance.6

All in all, the amount of money in Germany was raised too much in a short term. At the same time, consumer goods were not easily available due to insufficient production and job cuts.4 This resulted in steep inflation, which ended up destroying the Papiermark in November 1923.7

Figures from the German hyperinflation

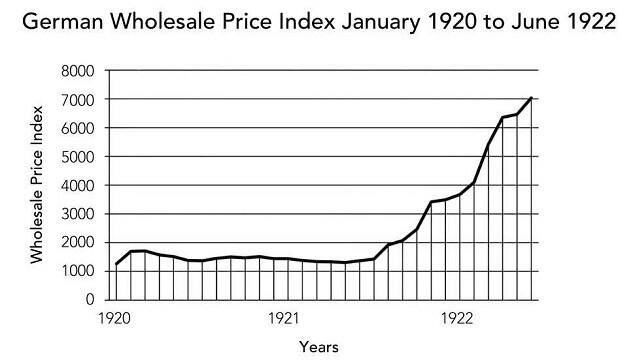

The German state ended up creating so much paper money that in 1923 the printing was conducted with the help of a total of 30 paper factories, almost 1,800 printing presses and 133 companies.6 For example, the financing of the Ruhr resistance was supposed to be merely a temporary solution, but along with other war financing, it clearly boiled over.

In October 1923, Germany's tax revenues covered only 1% of the country's expenditure. The remaining 99% were financed through printing money. In the middle of November 1923, 99% of short-term government debt was in the central bank's portfolio, and an additional 40 trillion marks in private commercial bills. 400 trillion marks' worth of cash were also in circulation in the same year's November, and simultaneously the state issued an equivalent amount of so-called “emergency money”.

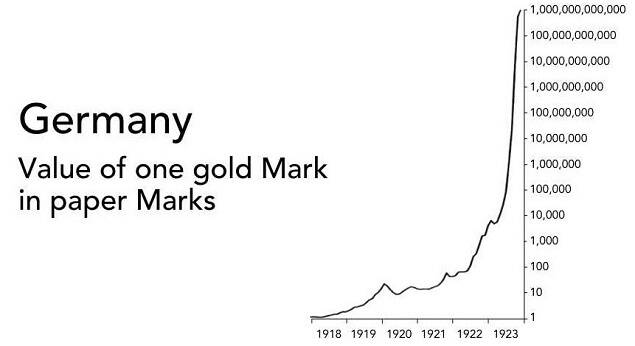

As a result, 1 kg of rye bread, which cost 163 marks in January 1923, cost 233 billion marks in November 1923. In May 1923, the exchange rate between the US dollar and German mark was 1:47,670, while in November 1923 it had inflated to 1:4,200,000,000,000.4 With this exchange rate, the above-mentioned 40 trillions' worth bonds would have amounted to $9.5, which corresponded to 13 grams of gold back in the day.

Assets during the German hyperinflation

Stocks

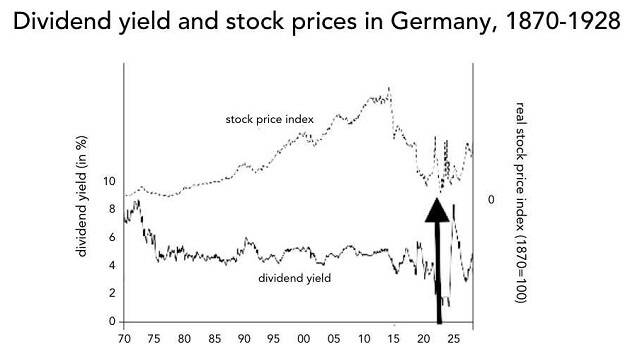

In 1920 and 1921, the stock market rose nominally, meaning that the value of stocks increased numerically. In reality, the losses were bigger than profits, since the value of money had weakened considerably, which meant that you could buy less with that money.

Back then, the stock market got the hopes high for many, which resulted in a nearly year-long boom that tripled the nominal prices of stocks. At the time when the German mark collapsed at the end of 1921, the stock market provided at least some sort of protection against the weakening currency.

However, this protection was only momentary, since in October 1922 the German stock market lost 97% of its value compared to the year 1913. The stock market could thus not act as the hoped-for safe haven against the weakening of the currency.8

Eventually, the valuation of German stocks in 1921–1923 was low, since there was great fluctuation in stock prices. The prices could change even 30–50% per month, until the stock market finally crashed in 1923.9

Bonds

General information about bonds

When you invest in bonds, you provide the capital in advance, for which you expect a fixed interest after an agreed period of time. The interest rate is the reward for the investor for the loan they give out. At the same time, the interest is the price that the lender pays for using the money in advance.

If inflation increases between the bond's date of issue and the date of repayment, the investors become less attracted towards the bond. This happens if the inflation is higher than the interest rate of the bond, since then the yield for the bond is lower than the increase in the cost of living. In other words, the bond's holder loses purchasing power. Even though many investors believe bonds to be a predictable source of income, periods of high inflation drain their profits—this is called the inflation risk.

Example: The fixed interest rate for a bond is 4%. At the same time, inflation is 3%. This means that the real returns for the bond is 4%−3%=1%.

The higher the inflation and the bigger the expectations for the inflation, the bigger the bond's interest must be for the investors. In hyperinflation, the inflation figures are over 50% a month, meaning that bonds usually amount to nothing.

There are also bonds that include inflation protection. The challenge with these is that the protection is determined by a consumer price index and the price level changes related to this index. The question is, how well can a consumer price index reflect the real level of inflation.

Bonds in the German hyperinflation

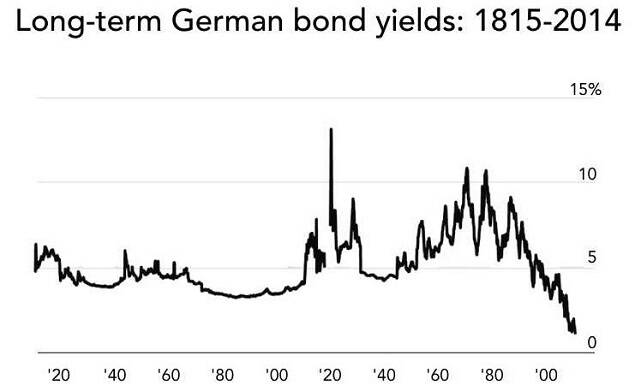

Germany issued wartime bonds in order to finance World War I. Hyperinflation wrecked the value of these bonds, since their interest rates could not keep up with the inflation. Thus inflation consumed the value and interest yield of the bonds.

As can be seen from the graph above, the yields for 1922 and 1923 have been omitted altogether. This is because the bond markets and the German mark were in such a chaotic state that there was little point in calculating the yields.10

Housing

What is common among countries who suffer from hyperinflation is their tendency to set price caps. For example, the German state regulated the price levels of rents in 1922–1923, and thus the local housing markets were destroyed. Rents could not be increased quickly enough to keep up with the accelerating inflation, which meant that the profits of apartment owners were destroyed and business became unprofitable.

The housing markets quickly became a non-profitable investment, because the rents could not be increased. At the same time, the maintenance costs of apartments swelled alongside other products and services. Many landlords' apartments stopped yielding profit, since the rents could not be used to cover the overhead costs. This eventually resulted in the relinquishment of apartments.

Gold

Gold fared the best during the hyperinflation when compared with the other assets, since gold's purchasing power rose exponentially. For example, when the hyperinflation was at its highest, you could have bought a block of commercial real estate in Berlin for 25 ounces of gold (which corresponded to $500 at the time).11 For the sake of comparison, the commercial premises in central Helsinki today could be sold for €400M, as was the case with the Stockmann shopping centre in spring 2022.12

Those who kept their wealth in the local currency or in other assets grew poorer, as the dreadful monetary policies of the government and the ensuing money creation ruined the German mark. Those who already back in 1918 had exchanged their German marks for gold or for the US dollar (that was in the gold standard) fared best during the German hyperinflation. Their purchasing power lasted even through the market crash, and gold also later gave them the opportunity to buy very cheap stocks or apartments after the crash.

Upon examining the price indices in post-WW1 Germany, you can notice that there is a parabolic move upwards, like in the graph below:

Yet if you look at a chart with prices measured in gold (such as above), they are remarkably more steady in comparison. In other words, products and services could be bought with gold throughout the German hyperinflation, whereas the purchasing power of the local currency was entirely ruined. This is one indication of the protection given by gold and its usefulness as a measure of value.

A viewpoint to be considered here is that with the same amount of gold you can get the same amount of baskets of bread, whether you were in hyperinflationary Germany or for example in France. Gold is a supranational asset, which means that it is unaffected by local crises. The German hyperinflation was particularly a problem of Germany, whereas gold carries purchasing power in all countries of the world.

Summary

The German hyperinflation was caused especially by the lackadaisical monetary policies of the German government. The German mark was delinked from the gold standard, which meant that an unlimited amount of money could be printed. However, the production was mainly focused on war equipment, whereas the civilian goods were undersupplied. The citizens had ostensibly a lot of money, but there were too few essential goods. The prices of these essential goods rocketed, and people were ready to pay more and more for them. The general price levels shot up, and the inflationary period that began in 1914 finally escalated into hyperinflation, which destroyed the German mark.

During the years of hyperinflation from 1921 to 1923, the wisest choice was to own gold. The nominal value of stocks rose at the beginning of this period, but since the value of money plummeted, the seeming profits did not help the investors in real life. The interest earned from bonds could not keep up with the hyperinflation, and the growing overhead costs of apartments could not be covered with rental income. It goes without saying that any money kept on a bank account during the period could not be spared from losing its value. Gold on the other hand retained its value.

Since gold is a supranational asset, it was not tied to the German markets, and thus it kept its value even throughout one of the worst hyperinflationary crises in the modern world.

Gold ownership is worth it

Fortunately, nowadays it is much easier to own gold than in early 20th-century Germany. For example, with Voima Account you can buy and sell gold whenever you want. With the mobile application, you move away from local currencies and protect your wealth with an asset that has withstood the ravages of history.

Open a Voima Account now! Alternatively, in Finland you can buy gold bullion and coins at Voima Store!

The views expressed on this post are those of the author and do not necessarily reflect the official views or position of Voima.

You are allowed to copy our content, in whole or in part, provided that you give Voima proper credit and include the appropriate URL. The name Voima and a link to the original post must be included in your introduction. All other rights are reserved. Voima reserves the right to withdraw the permission to copy content for any or all websites at any time.

Nothing written in Voima's blog or website constitutes investment, legal, tax or other advice. It should not be used as the basis for any investment decision which a reader thereof may be considering. The purpose of Voima's blog is to provide insightful and educational commentary and is not intended to constitute an offer, solicitation or invitation for investing in or trading gold.

-

https://www.ecb.europa.eu/stats/macroeconomic_and_sectoral/hicp/html/index.fi.html ↩

-

https://www.investopedia.com/terms/h/hyperinflation.asp#:~:text=Hyperinflation%20is%20a%20term%20to,more%20than%2050%25%20per%20month. ↩

-

https://lawliberty.org/monetary-lessons-from-weimar-germany/ ↩

-

https://www.historisches-lexikon-bayerns.de/Lexikon/EN:Inflation,_1914-1923 ↩

-

https://www.businessinsider.com/weimar-germany-hyperinflation-explained-2013-9?r=US&IR=T#but-regardless-of-the-politics-by-christmas-1921-ordinary-germans-were-feeling-the-squeeze-of-inflation-14 ↩

-

https://www.history.co.uk/articles/just-print-more-money-history-s-worst-cases-of-hyperinflation ↩

-

https://www.historisches-lexikon-bayerns.de/Lexikon/EN:Inflation,_1914-1923 ↩

-

https://newworldeconomics.com/hyperinflation-in-germany-2-the-stock-market/ ↩

-

http://www.crei.cat/wp-content/uploads/users/working-papers/voth_withabang.pdf ↩

-

Homer, Sidney & Sylla, Richard 2011: ‘A History of Interest Rates'. ↩

-

https://www.atlasvaults.com/modern-times-the-weimar-republic/ ↩

-

https://www.iltalehti.fi/talous/a/b857675a-5c3e-48e2-8432-90edef26b360 ↩