Gold in crises part 2: Great Depression

Lasse Lindholm

Community Manager

Table of contents

Introduction

This article series discusses how four of the most common assets have performed in four crises of recent history. The aim of the article series is to provide a background for the crises and give the reader an opportunity to protect their wealth today by using historical data.

The assets under review have been picked based on how common they are, namely stocks, bonds, housing and gold. For example forests and art have been left out, since they are not as relevant to common investors as the other assets: forests require a lot of maintenance, and art-as-investment usually has to do with very valuable, unique works. Art is also not valuated on the markets, but artworks are unique, which means that the unique characteristics of a work of art affect its value.

The reviewed assets are all local, meaning that for example in the case of Germany, we will only cover German investments.

The article series will discuss the following crises:

- German hyperinflation

- Great Depression (1930s)

- Stagflation in the 1970s

- Russo-Ukrainian War

The subjects under discussion involve essential factors in great economic crises, and all of them have taken place in a modern, developed economy. In addition, the Russo-Ukrainian war was included due to its topicality.

This article is about economic depression—that is, a deep prolonged recession. The historical focus here is on the Great Depression of the 1930s, which began in 1929 in the US and lasted for a decade. During this time, it escalated into a global crisis.1

The article sheds light on the economic circumstances before and during the Great Depression and what happened to the most common assets during the crisis.

Deflation and depression

Economic depression is a period of sustained contracting or slowing down of the economy. A depression can emerge either in a deflationary or inflationary environment, which means that the general price levels can either be on the decrease (deflation) or on the increase (inflation). This article focuses on deflationary depression. We will cover inflationary depression (or stagflation) in the next part of the series.

Deflation is the case when there is too much supply compared to the demand, when there is an increase in the demand for money or when there is a decrease in the supply of money or the availability of credit.

When production slows down as a result of lowered demand, and unemployment generally goes up, an economy can end up in a sustained recession, i.e. depression.

Let's take a look at an example of how deflation can escalate into a depression.

Europe will be facing a deflationary problem in the future when the baby boomers retire from the working life. This is because when people retire, they generally earn less and also spend less money on services. Pensioners produce less than workers, which means that the economic activity is contracted; i.e. the gross domestic product decreases. (The GDP measures the size of an economy, that is, the total value of a country's production under a certain period, often on an annual basis.)

The retiring people also generally sell their assets like stocks, bonds and houses in order to finance their retirement. If a lot of people sell these things simultaneously, there might be deflation: if there are a lot of sellers (supply) in the market at the same time but not enough buyers (demand), this leads to the decrease in prices.

There is another disadvantage to mass retirement. When the baby boomers turn pensioners, more workers are needed to fill in the vacancies. During this transition, the retiring full-time employees exit their jobs and they are replaced with probationary employees, whose income can be very uncertain during the trial period. Pensioners draw smaller sums of money than they earned back in the working life, and the probationary employees will not earn a corresponding amount given that they're just starting at their jobs. Because most of the working force gets a smaller pay, this decreases their consumption for the time being and their ability to take up a bigger loan to buy vehicles or real estate. If this kind of development takes place regularly and if every year the amount of people retiring exceeds the amount of people replacing them, this leads to a vicious deflationary circle or, in the worst case scenario, an economic depression.

As a case example, when Finland had an economic depression in the 90s, the unemployment figures were high and the budgetary deficit grew with startling speed. The financial crisis was also reflected as a bank crisis, since the unprecedented credit losses were threatening the solvency of Finnish banks. The Finnish government and the Bank of Finland had to support the banks with a total of 50.2 billion Finnish marks2, while the annual revenue of the government was only about 20 billion Finnish marks3. Immediately upon the outbreak of the crisis, the Bank of Finland had to take control of the third-largest commercial bank in Finland known as SKOP.

The Great Depression

The pre-Depression developments in the US

The decade preceding the Great Depression was a flourishing time for the economies of the US and the West. The main drivers for the economic boom of the 1920s were the post-WW1 recovery in consumption, the boom in the construction industry and the rapid popularisation of consumer goods such as cars and electricity in North America, Europe and other developed nations, such as Australia. This period was generally known as the Roaring Twenties.

The 1920s saw massive developmental leaps in the car industry and commercialisation of air traffic, telephones, videos, radios and other electronics, to name a few. The accelerating industrialisation overall heralded quick economic growth in the West, which further increased the need for consumption and for goods that could be used in new trending lifestyles and cultures.

The economic growth of the US was largely based on mass production, and its citizens adopted the new culture of consumerism. Furthermore, the troops returning from the battlefront were back in the job market, and the munitions factories began to produce consumer goods instead of armaments. The losing countries of WW1 also had to pay reparations to the US.

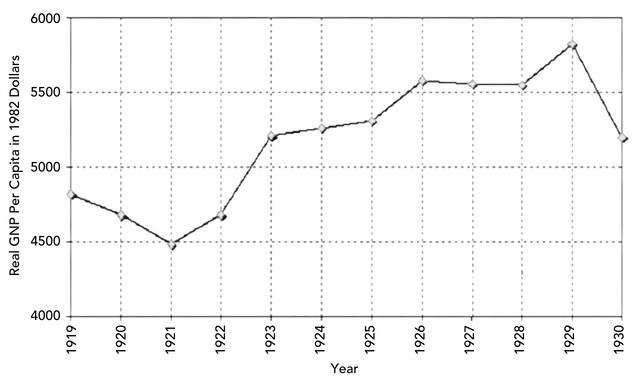

As a result, the gross national income of the US rose from $4,500 to $5,800 per capita between 1920–1929. (The gross national income differs from GDP in that GNI takes into account the total value of products and services of the country's residents, whereas GDP does not differentiate between citizens and non-citizens.)

Leveraging was especially easy back then, since the US central bank (founded in 1913) began to practise a new monetary policy that enabled low interest rates during the 20s. Thus the 1920s marked a watershed moment not only for culture and industry but also for investing. During this time, great amounts of debt were used to leverage the investments, in expectation of maximal profit from the bullish market.

It is very telling that back in the 1920s everyone had leveraged their portfolios to the max, regardless of whether they were millionaires, housewives, cleaners or cooks. People grew accustomed to the bull market and took up loans for their investments. The investors believed that the investment income would be great enough to well cover the repayments.

Many people were ready to risk their savings at the bullish stock markets. This resulted in an explosive growth at the market, which continued all the way up to 1929—and came crashing down.

From boom to bust

In 1929, the production had begun to splutter and the unemployment rates were on the increase. This was a consequence of the bad and sluggish monetary policy of the US central bank.

In 1928 and 1929 the US central bank made the decision to raise its key interest rate. By doing this, the central bank tried to restrict the use of leveraged debt in the security markets. As a result, the US economy slowed down and the production decreased, which resulted in increased unemployment. In the summer of 1929, the US economy was in a recession, because consumption slowed down and the consumer goods that were left unsold began to pile up, which further forced factories to cut down their production.

However, the stock prices continued to soar regardless. They reached figures that could no longer be justified by the expected performance of the US companies. In other words, the stocks were way overpriced.

As the markets began to react to the overpricing simultaneously, this caused a panic: stock owners began to frantically sell their overpriced securities to avoid losses. Eventually on 24 October 1929, there was a great surplus of sellers of overpriced stocks compared to the buyers, and the prices plummeted—the market crashed. The day came to be known as Black Thursday, since when the stock exchange opened in the morning, the stocks had lost over 11% of their value. A record number of stocks were sold on Black Thursday: 12.9 million stocks, which was triple the number commonly traded in the exchange.4 The market continued to fall, and next Tuesday an even greater number of stocks were sold, rendering millions of securities worthless. Those investors, who used a lot of leverage, were the ones who suffered most.

The situation was naturally extremely serious for the banking sector. This was made worse by disagreements among the Fed directors about how and by how much the central bank should support financial institutions. Some directors thought that all commercial banks should be aided. However, the majority was of the opinion that the support should be funnelled only to those commercial banks who were members of the central bank. This was once again a monetary policy mistake.

The decision brought about a wave of bankruptcies in the banking sector, because people were withdrawing their money from the non-member commercial banks, who could not afford the bank run. Concurrently, citizens were hoarding cash and banks lent out less and less money, which meant that the money in circulation decreased. From autumn 1930 to winter 1933, the amount of money in circulation dropped almost 30%.5

In turn, the diminishing supply of money decreased the average prices of goods and services. Simultaneously, the debt burden of people grew larger, since the money to be repaid had become more valuable through deflation. Deflation also distorted the economic decision-making, lessened the consumption of individuals and companies, worsened unemployment and made banks, companies and individuals insolvent. By 1933, when the Great Depression reached its nadir, approximately 12.8 million Americans were unemployed5 and nearly half of the US banks had collapsed.6

The effects of Great Depression elsewhere in the world

The Great Depression was the worst economic contraction in the history of the industrial world, which took place in 1929–1939. The triggering event is generally regarded to be the October 1929 stock market crash, which had Wall Street panicking while millions of investors were wiped out of the exchange.

A general deflation hit economies globally. In the following years, bankruptcies, bank crises and unemployment grew to unprecedented proportions in many countries. Once the Austrian bank Credit Anstalt went under, an international banking crisis flared up. During the next few years, consumption expenditure and investments shrunk, which occasioned a steep decline in industrial production and employment figures. As the economy contracted, the companies who operated at a loss were cutting down their staff heavy-handedly.

Asset performance during the Great Depression

Stocks

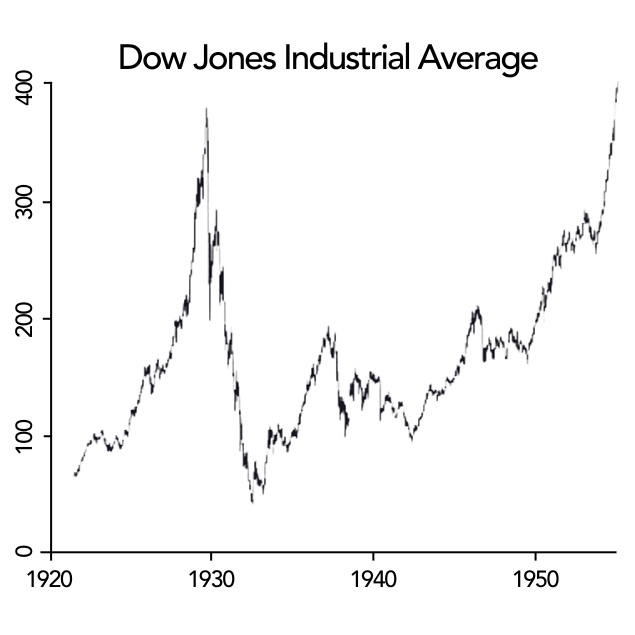

Many were extremely hopeful towards stocks since the stock markets had been going up for almost a decade (1920–1929). As an example, during this period the value of the Dow Jones index grew sixfold. Dow Jones includes 30 prominent industrial companies of the US (and the 1920s is particularly known for the Second Industrial Revolution). Many invested their savings in stocks, used leverage and even financed their investments by taking credit. The expectations for the market ran high.

That's why the state of the US economy and the effects of bad monetary policy took many investors by surprise. The stock market reached a bubble, and the stocks were overpriced when compared to the real profits made by the listed companies. The US had entered an economic recession, and the market reacted strongly to this: the indices dropped by many dozen per cent a day. On Monday, 28 October 1929, Dow Jones dropped by 13%, on the next day 12%, and mid-November 1929 its value had halved.7 The negative trend continued all the way to 1932, when Dow Jones had gone down 89% compared to its top figures. Ultimately, it took 22 years for the index to climb back to its pre-collapse heights.7

Stocks were not able to store wealth or act as a safe haven during the Great Depression. The stock markets were in chaos, and many investors lost their purchasing power.

Bonds

Bonds could not bring protection for investors because currencies were devalued during the Great Depression. Since the US dollar was in the gold standard, in practice the devaluation of the dollar meant that 1 US dollar corresponded to a smaller amount of gold than before. In this case, you could get 41% less gold with your buck.8 In other words, everything that was invested in US bonds weakened 41% in its value overnight.

This had grave implications for those who had invested in bonds, both in and outside the US: the institutions, such as central banks, who had invested in the US bonds lost their purchasing power. If the losses were too great, the decrease in the value of bonds could at worst make the foreign central banks devalue their own currencies. The worst-case scenario for this in turn was that the commercial banks in these countries would go under, as their debt burden grew intolerable through the currency devaluation.

Housing

In the Great Depression, the interest rates for mortgages rose and the issuing of loans decreased. The housing market slowed down and had a lot of debt involved, which eventually led to a drop in the housing prices. Between 1929 and 1933, the building of residential property in the US lessened by 95%9 and the repair expenditure fell from $50M to $500K. In 1932, approximately 250,000–275,000 people lost their houses to foreclosure; the figures were dramatic compared to 1926, when the number was 68,000. In 1933, over 1,000 suffered foreclosure daily. Housing prices dropped by approximately 35%, which meant that an apartment whose value was $6,000 pre-Depression, was worth merely $3,900 in 1932.9 The stark decline in housing prices also meant that the mortgages many people had in 1930 exceeded the value of their housing.

In practice, there was no market for the foreclosed housing units. Even if there were some individuals who were willing to buy them, they offered to pay such a low price that would only rarely cover the mortgage. This caused an additional strain for the banks and made the depression worse.

Gold

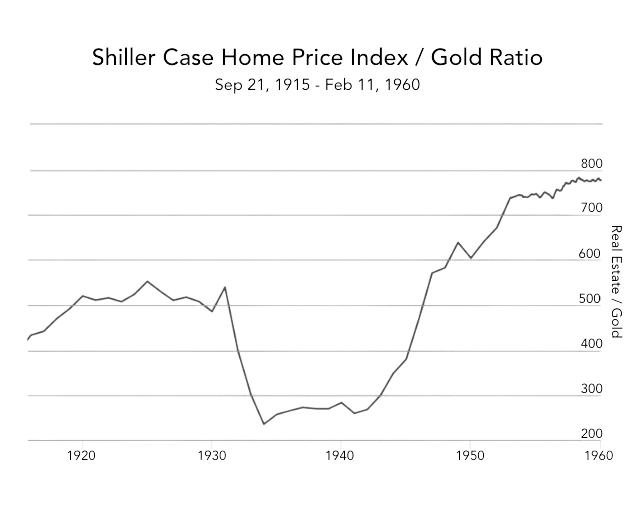

Gold performed well globally, since gold represents a safe haven when the times are in political or economic turbulence. During the pre-Depression times, citizens could exchange their greenbacks for gold. Those, who exchanged their paper money for gold before the dollar's devaluation, were the ones whose purchasing power was kept best. This was further reinforced if they also made use of their purchasing power by buying cheap stocks and real estate. The US dollar was devalued in 1934, which meant that gold rose in value: the ounce price of gold was changed from $20.67 to $35.

As an example of retained purchasing power: if we compare the price of real estate in 1931 and 1934, you could have bought a double amount of real estate with the same amount of gold.10

Summary

The main cause for the Great Depression was the massive amount of debt in the stock markets, which was enabled by the US central bank's new monetary policy of low interest rates throughout the 1920s. Low rates encouraged people to gratuitous risk-taking, and when the central bank finally raised its rates, the stock bubble—that was inflated by cheap debt—burst. When the rate was increased, people wanted to take up less loans, which led to a decrease in investments and consumption. Since the production had been growing unprecedentedly before this, the lessening consumption meant that plenty of products were left in warehouses, which ultimately led to companies doing layoffs.

Simultaneously, the stock markets had too much leveraged debt. When people ultimately wanted to sell their grossly overpriced stocks, they could not find enough buyers, and so the US stock exchange crashed within a short period (more than once). The markets continued to spiral down until 1932, by which time the Dow Jones index had plummeted 89% from the top figures. Bonds proved to be an unprofitable asset class due to global devaluations, since the money to be repaid had less purchasing power than the money lent. The housing market was also in the eye of the storm: in 1932, approximately 250,000–275,000 people lost their houses to foreclosure (cf. 68,000 in 1926). Simultaneously, the housing prices fell—the drop was about 35% in 1933 alone.

Gold performed best out of the four assets because within a short period of time, gold practically doubled its purchasing power in the housing market.

The views expressed on this post are those of the author and do not necessarily reflect the official views or position of Voima.

You are allowed to copy our content, in whole or in part, provided that you give Voima proper credit and include the appropriate URL. The name Voima and a link to the original post must be included in your introduction. All other rights are reserved. Voima reserves the right to withdraw the permission to copy content for any or all websites at any time.

Nothing written in Voima's blog or website constitutes investment, legal, tax or other advice. It should not be used as the basis for any investment decision which a reader thereof may be considering. The purpose of Voima's blog is to provide insightful and educational commentary and is not intended to constitute an offer, solicitation or invitation for investing in or trading gold.

-

https://www.imf.org/en/Publications/WEO/Issues/2016/12/31/World-Economic-Outlook-April-2009-Crisis-and-Recovery-22575 ↩

-

https://www.eduskunta.fi/FI/vaski/selonteko/Documents/vns_4+1999.pdf ↩

-

https://www.veronmaksajat.fi/luvut/Tilastot/Julkinen-talous/Valtion-tulot-ja-menot/#955c5690 ↩

-

https://www.federalreservehistory.org/essays/great-depression ↩

-

https://www.history.com/topics/great-depression/great-depression-history ↩

-

https://www.federalreservehistory.org/essays/stock-market-crash-of-1929 ↩

-

https://www.forbes.com/sites/nathanlewis/2014/07/17/devaluations-of-the-1930s-dont-justify-todays-funny-money-excess/ ↩

-

https://www.encyclopedia.com/education/news-and-education-magazines/housing-1929-1941#:~:text=Housing%20values%20dropped%20by%20approximately,reduced%20value%20of%20their%20home. ↩