Voima Markets Newsletter—November 2022

Sam Laakso

Head of Voima Markets

Currency market table

The weakest currency of the month in October was the Japanese Yen (JPY)

| Gold price in | October | 3M | YTD | 1Y | 3Y | 5Y | 10Y | 20Y |

|---|---|---|---|---|---|---|---|---|

| JPY | 1.09% | 2.16% | 15.42% | 19.49% | 48.58% | 68.15% | 77.02% | 523.93% |

| CHF | −0.17% | −2.22% | −1.97% | 0.16% | 9.55% | 28.93% | 2.11% | 248.45% |

| AUD | −1.51% | 2.01% | 1.32% | 7.65% | 16.24% | 53.66% | 53.89% | 345.63% |

| USD | −1.60% | −4.53% | −10.68% | −8.40% | 7.93% | 28.47% | −5.05% | 413.88% |

| SEK | −1.98% | −1.22% | 8.92% | 17.56% | 23.28% | 69.08% | 57.78% | 519.03% |

| EUR | −2.44% | −2.90% | 2.70% | 7.11% | 21.71% | 51.30% | 24.43% | 414.91% |

| CAD | −3.05% | −0.94% | −3.69% | 0.74% | 11.73% | 35.83% | 29.45% | 349.19% |

| GBP | −4.24% | −3.29% | 5.34% | 9.32% | 21.74% | 48.74% | 33.48% | 600.97% |

| NOK | −6.11% | −0.02% | 5.31% | 12.67% | 21.94% | 63.35% | 72.95% | 617.86% |

Top news in the markets recently

Record central bank buying lifts global gold demand, WGC says (Reuters)

ECB must keep raising rates even if recession risks rise, Lagarde says (Reuters)

Japan unveils $200 billion in new spending to ease inflation pain (Reuters)

Trader's comment 3 November 2022

Central bank gold demand hits an annual record already in September

Central bank gold purchases reached their highest annual level in 55 years—an annual record already in September. Some of the biggest buyers in Q3 2022 were Turkey, Uzbekistan and India. Note that these are not Western but rather Eastern central banks.

Eastern central banks have been buying gold ever since the end of the financial crisis of 2008, when the global monetary system came to the brink of collapse. The financial crisis of 2008 was the result of excessive debt and poor government policies. Now more than a decade later, not much has changed in terms of government policy: there is more debt in the economy than ever and the financial system is again in distress because of all this.

Eastern countries like China, Russia, India, Kazakhstan, Turkey and many more have been buying gold over the past decade, and in doing so, these countries have been preparing for the inflationary crisis we are experiencing now and which, I argue, will lead to a broad currency crisis where currencies lose their purchasing power a lot more than what we have seen so far.

Now might be the time to read my thesis' chapter 4.3 Third Scenario: Monetary System Reform.

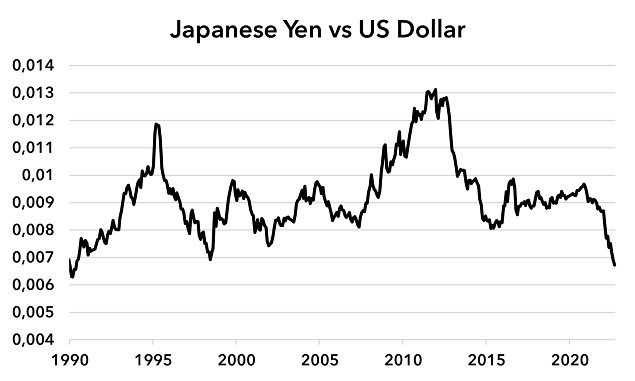

What's going on with the Japanese Yen?

The only major currency in which gold was up in October was the Japanese Yen and, as you can see, gold is up almost 20% this year against the yen. So what's going on in Japan?

For years, central bankers and economists have been pointing at Japan in defence of the extraordinary money creation Western central banks have been doing. The argument has been that central banks can create money out of thin air and lend it to governments at negative or zero interest, and even though the governments spend the money on goods and services, this will not cause inflation—or in other words the depreciation of the currency the central bank is creating.

As a result of this theory, Japan has become the most indebted country in the developed world by all measures and one of the favourite case examples for the economists who support this theory. So far this has not been an issue for Japan as interest rates have been low all across the globe, but this year the situation has changed.

Unlike central banks in other developed countries, the Bank of Japan has not been raising its benchmark interest rate this year. The Bank of Japan's governor, Haruhiko Kuroda, has repeatedly claimed that the economy of Japan is too weak to handle higher interest rates.

Japan has experienced economic and currency stability over the past 20 years despite the excessive debt taking, but now Japan stands in a situation where the economy of Japan can't handle higher interest rates (businesses would go bankrupt), the government of Japan can't afford higher interest rates (the government would have to default on its debt) and now other major central banks are hiking their interest rates extremely quickly. On top of this, Japan has an immense demographic problem as the population is ageing and the working age population of Japan has been shrinking since 1995.

Japan is a walking zombie which is just barely getting along and finally now that other central banks have been raising interest rates, investors are getting better returns in other currencies and have been dumping the Japanese Yen—investors are looking to abandon the sinking ship called the Japanese Yen. It looks like debt weighs after all and, after years of excessive money creation, the Japanese Yen is feeling the gravity.

Like the Bank of England in September, the Bank of Japan has had to intervene multiple times in the currency markets this year to try and prop up its own currency—without much success. At the same time, the government of Japan has been ‘helping' its citizens cope with higher inflation by giving them free money in various stimulus programmes. So the Bank of Japan has had to create yens out of thin air, which are then given to the citizens to help cope with the falling value of the yen. Right, that should make it better.

Christine Lagarde—a prime example of incompetence

Speaking of doing a bad job, I'm astonished by the lack of criticism central bankers are getting—both for their actions and their incompetence—given the situation we are in. A prime example of this is the current president of the European Central Bank, Christine Lagarde.

In one of her latest public appearances on 28 October, Christine Lagarde said once again that the current inflation came from ‘pretty much nowhere'.

Let's pause for a minute.

As the head of the ECB, Christine has one job above all else, which is to maintain price stability in the eurozone—to keep consumer prices from rising too fast. Everything else is secondary to this mandate. Christine gets paid €450,000 a year for doing this job and she probably has the most human and economic resources in the world to study the economy in order to get this job done right. Yet, she calmly claims that inflation came from ‘pretty much nowhere'. You would expect her to be on top of the situation, right?

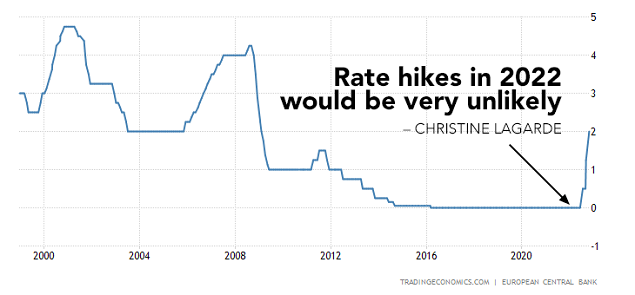

Back in December 2021, Christine made a clear prediction. She claimed that the EU inflation would be a passing ‘hump' and that rate hikes in 2022 by the European Central Bank would be ‘very unlikely'. So how did it go?

Now, eleven months later inflation in the eurozone is at an all-time high and we have seen the steepest rate hiking year the ECB has ever performed.

Despite being dead wrong on both inflation (her main job) and the amount of rate hikes the ECB would do this year (her main tool for doing the job), there is little criticism towards her and her colleagues. She is not the only central banker to be 100% wrong in the past few years, but the last year in particular has shown that she is in reality extremely unqualified for the job.

The way central bankers and most economists are still represented today—as the masters of their domain not to be questioned by common sense—is in my opinion distasteful and the fact that they are not held accountable for their blatant mistakes and clear incompetence, which is causing ordinary people to lose their life savings and their hard earned money, is inexcusable.

By the way, the markets do know that she's incompetent—that's why the euro has lost about 20% of it's value against the US dollar over the past year and a half.

Stocks

Quite many of Voima's wealthy Customers as well as institutional investors are asking our opinion about stocks—which is understandable, as stocks are often the part of investors' portfolio they are willing to touch if better opportunities arise. I'm not a stock guy but rather I like to look at things from a macro standpoint as macroeconomics is the main driver of all broad markets. This is also the case for one of the most economically sensitive asset classes, stocks.

If you've read my previous market comments and newsletter, I have no surprises for you—nothing has changed for stocks.

The macroenvironment is negative for equities and, based on the data available, is likely to stay negative until the end of at least H1 2023. US stocks are up about 10% from their October lows. The biggest bounce we've seen so far in this equity bear market was about 18% in July–August.

When the Dotcom bubble burst in 2000, the average rally was +15% and the average move to lower lows was −18%. In the 2008 financial crisis, the average rally was +12% and the average move to lower lows was −19%. The largest bear market bounce in the current bear market is +18%, in 2008 it was +23%, and in 2000 it was +21%.

A lot of people say they are bearish on stocks, but are they positioned that way? Most often they are not.

Gold

As you read at the beginning of this newsletter, Eastern central banks are buying gold hand over fist. Perhaps they are taking advantage of the lower gold prices, which have come about due to falling overall liquidity across markets—something I discussed in the October newsletter. That being said, the coming months remain challenging for gold, but if you are looking past this year and perhaps even past next year, I would argue that you should look at what the Eastern central banks are doing—and have been doing since 2008.

Other news

Voima Gold Talks November—Zoltan Pozsar

Zoltan Pozsar, who is the Global Head of Short-Term Interest Rate Strategy at Credit Suisse, will be the keynote speaker at Voima Gold Talks in Helsinki this month. Zoltan has raised eyebrows in the markets with his Bretton Woods III theory, in which he argues that the world will soon see a new world (monetary) order centred around commodity-based currencies in the East, which is also likely to weaken the euro and the dollar and will also contribute to inflationary forces in the West. You can find more about Zoltan's work online and you can also listen to Zoltan's interviews on Bloomberg's podcast Odd Lots.

Disclaimer

The views expressed on this post are those of the author and do not necessarily reflect the official views or position of Voima.

You are allowed to copy our content, in whole or in part, provided that you give Voima proper credit and include the appropriate URL. The name Voima and a link to the original post must be included in your introduction. All other rights are reserved. Voima reserves the right to withdraw the permission to copy content for any or all websites at any time.

Nothing written in Voima's blog or website constitutes investment, legal, tax or other advice. It should not be used as the basis for any investment decision which a reader thereof may be considering. The purpose of Voima's blog is to provide insightful and educational commentary and is not intended to constitute an offer, solicitation or invitation for investing in or trading gold.