Voima Markets Newsletter—February 2023

Sam Laakso

Head of Voima Markets

Currency market table

| Gold price in | January | 3M | 1Y | 3Y | 5Y | 10Y | 20Y |

|---|---|---|---|---|---|---|---|

| NOK | 7.67% | 13.49% | 20.44% | 31.59% | 85.61% | 111.74% | 654.69% |

| SEK | 5.97% | 11.78% | 20.20% | 31.48% | 89.96% | 90.23% | 536.19% |

| USD | 5.65% | 18.02% | 7.29% | 21.24% | 43.33% | 15.90% | 423.07% |

| JPY | 4.85% | 3.27% | 21.29% | 45.55% | 70.84% | 64.42% | 467.61% |

| CHF | 4.74% | 8.05% | 6.08% | 15.38% | 41.07% | 16.77% | 251.56% |

| EUR | 4.14% | 7.45% | 10.97% | 23.83% | 63.92% | 44.91% | 418.68% |

| GBP | 3.86% | 9.99% | 17.19% | 30.00% | 65.23% | 49.28% | 600.22% |

| CAD | 3.77% | 15.31% | 12.39% | 21.91% | 54.93% | 54.73% | 357.64% |

| AUD | 2.10% | 7.12% | 7.48% | 15.04% | 63.72% | 71.31% | 335.82% |

The weakest currency of the month in January was the Norwegian krone (NOK).

Top news in the markets recently

Central banks bought the most gold since 1967 last year, WGC says (Reuters)

Russia and Iran are working on a gold-backed cryptocurrency to take on the dominant dollar, report says (Business Insider)

Gold as International Reserves: A Barbarous Relic No More? (IMF Working Papers)

Trader's comment 8 February 2023

At the end of October last year, gold was extremely stretched to the downside as gold prices had declined consecutively for seven months. As a result, the sentiment in gold was extremely negative and you could hear analysts betting for lower and lower prices to come—even the World Bank released a commodity market outlook in October 2022 where it estimated that gold would fall 4% in 2023 and average 1,665 USD/oz in 2024. The negative sentiment was also evident from the bearish market positioning visible from ETF fund-flow and COT reports. Sentiment in October was as negative as during the major bottoms in gold in 2018 and 2015.

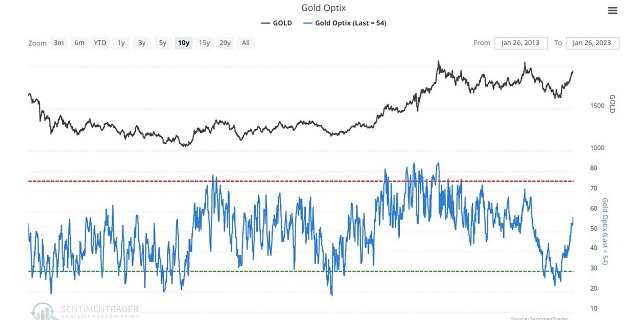

Now, over the past three months, gold has rallied against all major currencies. However, the sentiment in gold is still far from overly bullish, meaning that speculators are still quick to take profits and there is still lots of doubt. One of the most reliable sentiment metrics I've found is the Optix indicator provided by SentimenTrader which is based on their proprietary data model.

As you can see from the chart above, the sentiment in gold as measured by the SentimenTrader Optix indicator was extremely low late last year and has now bounced to neutral—although gold rallied over 20% against the US dollar and got to less than 6% from all time highs in three months. The market positioning as can be seen from the COT reports is also rather unenthusiastic.

As a contrarian, I would consider both of these as bullish indicators as they mean that there is still lots of money which is yet to chase gold higher despite the steep rally we've already seen.

Gold started a correction last week after the Fed's FOMC meeting. After an aggressive multi-month rally, a short-term correction lower is very healthy, and such corrections often flush short-term bulls from the market, resetting short-term sentiment, which in turn provides the fuel for the next leg up.

There is still plenty of room for sentiment and market positioning to get bullish on gold, and I'd say that it is likely that gold will find a short-term bottom within the next three weeks, after which we'll probably see another leg higher and new highs.

A short-term correction in gold, in which we are right now, should act as a great entry opportunity for those of you on the sidelines with gold. After two years of consolidation—in the US dollar price of gold—the multi-year trend in gold is turning positive and we are still very early in this rally. I think that it is reasonable to expect new all-time highs for gold in all major currencies during the first half of 2023—as we have already seen in GBP, JPY, NOK, and SEK.

USD

After diving below parity in September, the euro has bounced against the US dollar and the long euro trade has been one of the top consensus longs in macro for the past couple of months. However, given the fundamentals of the eurozone and the current global macroeconomic setup I would be cautious if I was heavily long euros against the US dollar. We are entering the liquidity crunching phase of this economic cycle, which tends to be a period of high asset volatility and bullish for the US dollar.

The big picture

Let's take a look at some of the big picture news in gold over the past year:

- Central banks bought over 1,130 tonnes of gold in 2022, the highest annual amount in 55 years, second highest on record, and double the average annual purchases from 2010 to 2021.

- Ghana crafted a policy which enables the government to start paying for petroleum product imports with gold.

- After getting heavily sanctioned, Russia has announced that it's planning for a gold-based payment system together with Iran.

Whether Russia or Ghana are successful in their gold-based trade initiatives does not really matter, because these are just some of the examples of the remonetisation trend in gold which has been developing since the global financial crisis of 2008.

The weaponisation of the US dollar through sanctions is driving developing nations to come up with alternative trade and payment systems, which need to be based on solid units of measure for which gold has been suggested by a number of nations over the past ten years. The will of these nations is quite clear but so far the attempts to create such payment systems have not been carried through.

The fact that central banks across the world have been accumulating gold ever since the global financial crisis, that these purchases have been accelerating, and even suggestions of gold- based payment systems by governments, should raise some questions, such as, why are they buying gold in the first place? We have examined the reasons in previous posts, and I would argue that these purchases remain the number one factor in the big picture which everyone should write down in their notebooks.

Stocks!

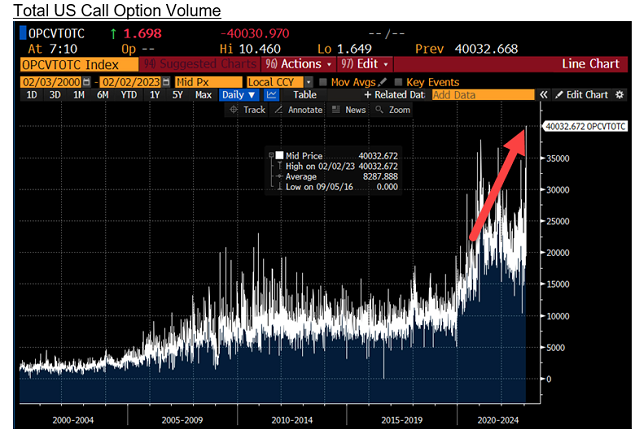

Increased activity in Call options (leveraged bullish bets) has been a characteristic of the stock market bubble which began to burst in November 2021, and call-option buying played a major role in the meme stock rallies of 2021. Highly leveraged long bets are typical of all major bubbles but the one in 2021 was extreme on many measures.

On Thursday 2 February, call-option volume in US stocks reached a new all-time high as stocks climbed after the FOMC meeting. Looking at the chart below, does this make you bullish? Given the macroeconomic environment we are in, I think that it shouldn't.

A steep decline in US stocks and global liquidity remains the number one risk for gold as discussed in the December market commentary.

Disclaimer

The views expressed on this post are those of the author and do not necessarily reflect the official views or position of Voima.

You are allowed to copy our content, in whole or in part, provided that you give Voima proper credit and include the appropriate URL. The name Voima and a link to the original post must be included in your introduction. All other rights are reserved. Voima reserves the right to withdraw the permission to copy content for any or all websites at any time.

Nothing written in Voima's blog or website constitutes investment, legal, tax or other advice. It should not be used as the basis for any investment decision which a reader thereof may be considering. The purpose of Voima's blog is to provide insightful and educational commentary and is not intended to constitute an offer, solicitation or invitation for investing in or trading gold.