Voima Markets Newsletter—August 2023

Sam Laakso

Head of Voima Markets

Currency market table

| Gold price in | July | 3M | 1Y | 3Y | 5Y | 10Y | 20Y |

|---|---|---|---|---|---|---|---|

| USD | 2.32% | −1.28% | 11.27% | −0.53% | 60.55% | 48.52% | 453.29% |

| CAD | 1.95% | −3.92% | 14.70% | −2.21% | 62.80% | 90.61% | 419.30% |

| EUR | 1,54% | −1.04% | 3.39% | 6.49% | 70.68% | 79.62% | 465.04% |

| AUD | 1.53% | −2.76% | 15.66% | 5.71% | 77.42% | 98.47% | 433.86% |

| GBP | 1.28% | −3.39% | 5.44% | 1.40% | 64.12% | 75.91% | 593.96% |

| JPY | 0.88% | 3.07% | 18.87% | 33.66% | 104.21% | 115.94% | 552.76% |

| SEK | −0.15% | 1.29% | 15.43% | 19.32% | 92.13% | 139.79% | 608.18% |

| CHF | −0.36% | −3.74% | 1.96% | −4.99% | 41.37% | 39.81% | 252.12% |

| NOK | −3.29% | −5.95% | 16.72% | 10.88% | 99.41% | 155.42% | 668.68% |

The weakest currency of the month in July was the US Dollar (USD).

Top news in the markets recently

Bankruptcy Filings Surge in First Half of 2023 in US, Epiq Says (Reuters)

China's Central Bank Adds More Gold for a Ninth Straight Month (Bloomberg)

Countries Repatriating Gold in Wake of Sanctions against Russia, Study Finds (Reuters)

Russia Confirms BRICS Will Create a Gold-Backed Currency (Kitco)

Trader's comment 10 August 2023

Voima Markets newsletters are back from the summer holidays, and in this month's release we'll take a brief look at some commodity charts, examine what they mean for inflation and what the macroeconomic setup looks like in the US and Europe.

Commodities and inflation

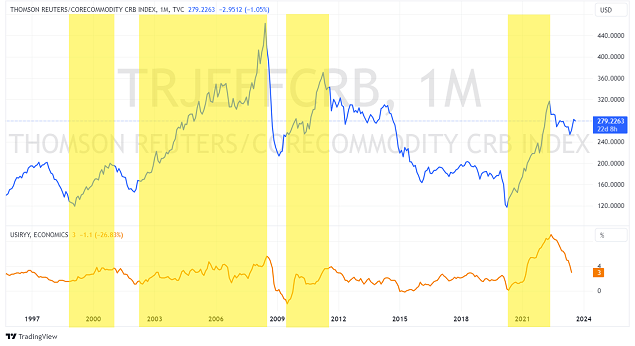

The Refinitiv/Corecommodity CRB index (formerly known as the Thomson Reuters Core Commodity CRB index)—or CRB in short—is a broad commodity index which weighs global economic significance such as consumption, production levels and trends in the weighing of different commodities. The index's highest weighing is in oil due to its extremely broad use cases and subsequent significance for the global economy. The index also acts as a proxy for inflation as rising commodity prices ultimately trickle down to consumer prices as we have all experienced especially over the past couple of years.

In July, the CRB index made a new multi-month higher high—rising above its April highs. If the CRB index proceeds into a trend of higher highs and, just as importantly, higher lows, that would suggest that inflation pressures have started to pick up again.

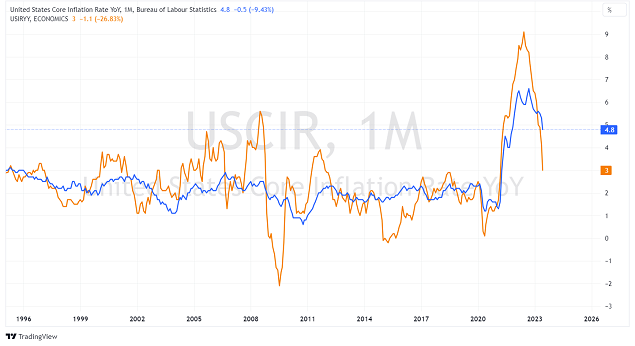

It is also worthwhile to note that core inflation, which does not take into account energy and food prices, has been a lot stickier compared to headline inflation so far. Now more recently, we are seeing some major energy and food components of headline inflation making higher highs—albeit these are inherently volatile components. Core inflation in the US is still 4.8% and 5.5% in the eurozone. With inflation having been elevated for more than two years, these year-over-year changes are starting to compound significantly, and now there seems to be a tailwind for even higher inflation.

As of yesterday, WTI crude oil futures have also surpassed April highs, indicating a major higher high. It remains to be seen whether this higher high is followed by a higher low which would further signal that inflation is accelerating.

In the bigger picture, commodities have been correcting and consolidating since the summer of 2022 and the commodity sector looks to be forming a long-term bottom, which the CRB index's price action is also indicating. Whatever the outcome may be, this is something that investors should keep a close eye on.

There is a case to be made that the commodity cycle is still very early and the setup has similarities to the 1970's commodity cycle in which inflation came in three waves. This would of course be a major challenge and headache for central bankers, who are trying to keep inflation at bay.

Market outlook

During the first half of 2023, US stocks rallied as the US GDP accelerated from 0.9% YoY in Q4 of 2022 to 2.6% YoY in Q2 of 2023, while at the same time inflation was still falling. This is an ideal environment for growth-sensitive asset classes like equities, and so the resilience of the US economy has surprised many—myself included. This is why it is always important to stay humble before data and the unknown.

Rate hikes over the past 18 months have not yet fully permeated the real economy, and it is not clear how well the global economy can cope with the “higher for longer” interest rates. Some signs of stress on the system include rising bankruptcy rates in major economies, several bank failures in the US, and many European economies including Germany, UK, Italy and Sweden are seeing no or negative GDP growth. Initial jobless claims in the US have also risen this year but remain at historically low levels still. As H2 progresses, we will see how resilient the US economy is for the rate hikes already in place.

Right now short-term economic data suggests that US GDP growth is unlikely to accelerate much further from here. The Fed is likely to keep interest rates high throughout the end of the year especially if inflation starts to reaccelerate and US GDP growth remains positive. The situation for the ECB is much less straightforward. European stocks performed well in Q1 but were mostly flat or down in Q2, and with growth continuing to slow in Europe, the outlook for European stocks is bleak.

So far this year, the euro has continued to make higher highs and higher lows against the US dollar but momentum has slowed substantially. The fact that the euro is struggling to maintain new highs—as has been the case in April and July this year—is a clear indication of exhaustion, and based on the data available today, the outlook for the euro relative to the US dollar remains negative for H2.

Gold is up by over 18% against the US dollar and over 6% against the euro from the October lows and, with falling volatility, the short-term setup suggests that gold will produce a higher low over the coming weeks or months—as discussed in the previous Voima Markets newsletter, with our end of the year outlook remaining unchanged.

The big picture

As with ocean tides, seasons and almost every aspect of life, periods of calm are often followed by periods of storm and vice versa. I am not trying to sound gloomy on purpose, but this is always good to keep in mind. Based on history, the exceptionally long and calm period after the global financial crisis is likely to be met with a balancing force of similar magnitude in the opposite direction.

Ray Dalio did a great job explaining the big picture in the US in his latest article titled ‘What's Happening with the Economy? The Great Wealth Transfer'—with which I dare not disagree.

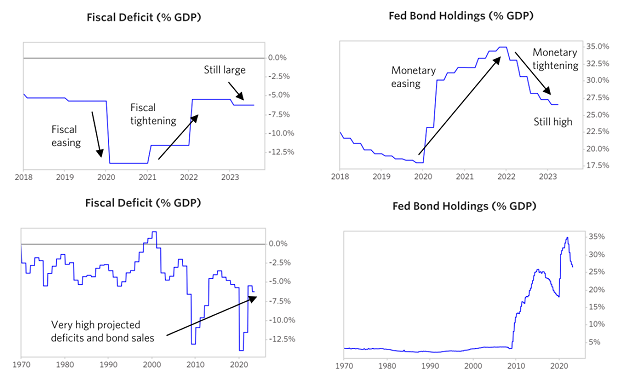

The next two pairs of charts show the US budget deficit (on the left) and the Federal Reserve's bond holdings (on the right). In them, you can see the massive deficits and the massive Fed bond purchases to fund these deficits in 2020 and 2021. In the ones on the left, you can see that these deficits are still large and tending toward worsening, and in the ones on the right you can see that, since the beginning of MP2 [current monetary policy environment] in 2008, the Fed accumulating bonds has been the norm, with two occasional and modest exceptions. I am watching this number closely because I believe the next significant increase in monetization will probably signal the last and probably biggest leg of the long-term debt cycle's reduction in the values and burdens of debts.

Ray Dalio

Disclaimer

The views expressed on this post are those of the author and do not necessarily reflect the official views or position of Voima.

You are allowed to copy our content, in whole or in part, provided that you give Voima proper credit and include the appropriate URL. The name Voima and a link to the original post must be included in your introduction. All other rights are reserved. Voima reserves the right to withdraw the permission to copy content for any or all websites at any time.

Nothing written in Voima's blog or website constitutes investment, legal, tax or other advice. It should not be used as the basis for any investment decision which a reader thereof may be considering. The purpose of Voima's blog is to provide insightful and educational commentary and is not intended to constitute an offer, solicitation or invitation for investing in or trading gold.