Voima Markets Newsletter—April 2023

Sam Laakso

Head of Voima Markets

Currency market table

| Gold price in | March | 3M | 1Y | 3Y | 5Y | 10Y | 20Y |

|---|---|---|---|---|---|---|---|

| NOK | 8.50% | 15.17% | 20.93% | 25.98% | 98.10% | 120.66% | 738.56% |

| AUD | 8.48% | 9.92% | 13.63% | 14.92% | 70.66% | 92.05% | 427.12% |

| USD | 7.79% | 7.87% | 1.58% | 25.26% | 48.63% | 23.29% | 483.12% |

| SEK | 6.82% | 7.54% | 12.23% | 31.58% | 84.90% | 96.12% | 616.37% |

| CAD | 6.76% | 7.60% | 9.84% | 20.41% | 55.83% | 63.81% | 436.81% |

| EUR | 5.15% | 6.50% | 3.67% | 27.42% | 68.90% | 45.75% | 487.51% |

| GBP | 5.15% | 5.80% | 8.14% | 26.09% | 68.86% | 51.92% | 648.35% |

| JPY | 4.96% | 9.25% | 10.88% | 54.69% | 85.74% | 73.81% | 556.09% |

| CHF | 4.68% | 6.74% | 0.72% | 19.26% | 42.62% | 18.83% | 294.84% |

The weakest currency of the month in March was the Norwegian krone (NOK).

Top news in the markets recently

The Digital Age Ushers in a Speedier, More Viral Breed of Bank Run (Bloomberg)

2-year Treasury yield posts biggest 3-day decline since aftermath of 1987 stock crash (CNBC)

Amazon to Cut 9,000 More Jobs, Deepening Biggest Pullback Ever (Bloomberg)

Union Bank Plaza in Downtown LA Sells at a Big Loss (Commercial Observer)

Blackstone REIT limits investor redemptions again in March (Reuters)

Trader's comment 5 April 2023

March was a tumultuous month in the financial markets, with a number of significant events taking place that are likely to keep causing ripples across the markets in the coming months. From the collapse of several US banks to a reported change in Russia's gold reserves, here are some key takeaways from last month.

Banking panic and central bank gold purchases

The collapse of several US banks was a major concern for investors in March. This was followed by the sale of Credit Suisse to UBS in a contentious deal that saw bondholders overridden by shareholders. These events caused considerable turmoil in the banking sector and raised concerns about the health of the financial system as a whole.

Although the immediate panic has now somewhat faded, it is worthwhile noting that during the 2008 financial crisis Bear Stern fell already in March 2008 whilst Lehman Brothers collapsed in September. It would be quite daring to say for certain that the worst is already behind.

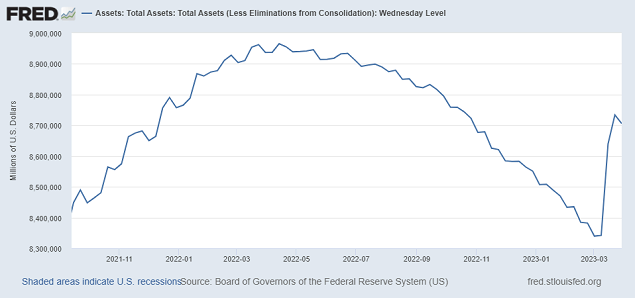

As a result of the banking panic, the Federal Reserve resolved to provide quantitative easing to the tune of $391B, erasing five months of quantitative tightening in just two weeks. Some economists would argue that technically this is not quantitative easing. Yet, the Fed's balance sheet keeps growing whilst according to their policy guidance their balance sheet should be shrinking by $95B per month. Taking a look at the chart below, everyone can draw their own conclusions.

On the other side of the world, Russia reported that its gold reserves were increased by 31 tonnes in 2022. This was the first time that Russia reported a change in its gold reserves since the start of the conflict. Russia's update is a continuation to the news that have been coming in from other Eastern countries which have also acted as buyers in the gold market. In addition to Russia, China, Singapore, India, Egypt, Qatar, Iraq, the United Arab Emirates as well as other smaller buyers have been active in the gold market over the past 12 months.

The real economy and real estate

Another noteworthy development in March was Amazon's decision to cut a further 9,000 jobs, after already cutting 18,000 earlier in the year—the largest layoffs in Amazon's history. Similar layoffs have come from a lot of other major companies like Microsoft and McDonald's. These are not good signs for the health of the real economy, and Amazon in particular is a good proxy for retail purchasing power and the health of the consumer.

The fact that the world's largest online retailer is shedding jobs at a record pace is a worrying indicator of economic conditions, and as we get into the Q1 earnings season, companies will be reporting the deteriorating economic conditions.

The situation in commercial real estate is also a cause for concern. Over the next 21 months, trillions of dollars worth of real estate debt in the US alone will need to be refinanced. This debt was last financed when interest rates were close to zero, but in just one year the cost of borrowing has exploded. It will cost a lot more to refinance these debts, potentially making some projects unprofitable and causing further liquidations in an already illiquid market.

The sale of Union Bank Plaza at a 50% loss is a prime example of how quickly profits in real estate can turn into major losses on paper. Another worrying sign of the commercial real estate bust is that the $70B commercial real estate fund BREIT had to limit withdrawals again in March. BREIT recorded $4.5B worth of withdrawal requests in March and could only fill 666 million—15% of the withdrawals. Generally speaking, it is probably not a bad idea to limit exposure towards real estate as a whole.

Market moves and outlook

It could well be that we will see a further escalation of the liquidity crunch that has been intensifying over the past few months. Q2 could get really ugly for equities and other growth-sensitive asset classes as companies report slowing growth in Q1 and losses related to the banking crisis which began in March.

In the face of all these challenges, it's important for investors to be prepared to make changes to their portfolios as needed. Stocks look precarious, even though we saw rallies towards the end of March. During a bear market in stocks, it is not unordinary to see so-called ‘month-end markups', meaning a rally towards the end of the month followed by the resumption of the bigger trend downward.

These anomalies are thought to be driven by hedge funds and money managers, who want to improve reported results, which are calculated on a month-end basis. Also, the markups tend to be bigger at the end of a quarter. Obviously month-end markups are not the only force driving prices higher during a bear market but the setup for US stocks is similar as it was in December 2021, March 2022, May 2022, November 2022 and January 2023.

The bond market is also pricing in a lot of uncertainty, with the US bond market volatility index MOVE hitting new record highs not seen since 2009, and the rising volatility in the US bond market to this day resembles the period from June 2007 to early 2008. In addition, it is worthwhile remembering that, historically, markets don't bottom when the Fed cuts rates for the first time but rather roughly 6–18 months after the first rate cuts.

In this environment, gold is a good asset to consider adding to your portfolio. Gold is the only financial asset that doesn't carry counterparty risk, which makes it an excellent hedge against economic uncertainty and during banking crises. While you shouldn't be all-in-gold in your portfolio, not having any gold at all is quite daring given the current economic environment.

I have been increasingly underlining the case for gold since December 2022 and will continue to do so for as long as the current macro environment supports the argument. I also continue to think that we will see fresh all-time highs in Q2. The World Gold Council released the Relevance of gold as a strategic asset 2023 report at the end of March, and it summarises quite well why one should consider a gold allocation over the longer term.

There is likely to be continued volatility in the markets as the year progresses, and by being aware of the events happening within the bigger macro economic cycle we are in, you can take steps to protect your wealth and be better prepared for whatever the future may hold.

PS. Amid the banking crisis in March, we released an article titled What is a bank run and how can it lead to a banking crisis?

Disclaimer

The views expressed on this post are those of the author and do not necessarily reflect the official views or position of Voima.

You are allowed to copy our content, in whole or in part, provided that you give Voima proper credit and include the appropriate URL. The name Voima and a link to the original post must be included in your introduction. All other rights are reserved. Voima reserves the right to withdraw the permission to copy content for any or all websites at any time.

Nothing written in Voima's blog or website constitutes investment, legal, tax or other advice. It should not be used as the basis for any investment decision which a reader thereof may be considering. The purpose of Voima's blog is to provide insightful and educational commentary and is not intended to constitute an offer, solicitation or invitation for investing in or trading gold.