Voima Markets Newsletter—September 2023

Sam Laakso

Head of Voima Markets

Currency market table

| Gold price in | August | 3M | 1Y | 3Y | 5Y | 10Y | 20Y |

|---|---|---|---|---|---|---|---|

| NOK | 3.66% | −5.18% | 21.59% | 20.07% | 104.82% | 141.77% | 630.92% |

| SEK | 2.80% | −0.25% | 16.54% | 24.72% | 93.36% | 129.88% | 575.86% |

| AUD | 2.33% | −0.83% | 19.58% | 11.99% | 79.11% | 90.65% | 415.76% |

| CAD | 1.15% | −1.62% | 16.67% | 1.96% | 67.37% | 78.21% | 403.18% |

| JPY | 1.01% | 3.24% | 18.75% | 35.34% | 111.77% | 106.07% | 543.02% |

| EUR | 0.15% | −2.55% | 5.15% | 8.38% | 72.78% | 69.42% | 422.91% |

| CHF | 0.04% | −4.12% | 2.45% | −3.75% | 47.29% | 32.00% | 225.72% |

| GBP | 0.01% | −2.98% | 3.95% | 3.85% | 65.16% | 70.01% | 542.67% |

| USD | −1.24% | −1.15% | 13.39% | −1.52% | 61.55% | 38.98% | 416.48% |

The weakest currency of the month in August was the Norwegian krone (NOK).

Top news in the markets recently

Moody's downgrades US banks, warns of possible cuts to others (Reuters)

China lifts temporary curbs on gold imports as renminbi recovers (Financial Times)

Gold Demand Trends: Gold continues to perform as central bank buying hits H1 record (World Gold Council)

Trader's comment 19 September 2023

Following up on the August newsletter, inflation continues to accelerate in the US, rising from from 3.2% to 3.7% in August. Commodities have continued to rise, with the CRB making a big time higher low in August and pushing to new higher highs in September. The move has been driven largely by oil, which is the most important commodity for the global economy and has rallied more than 40% from the summer lows so far.

With the data at hand, it seems more likely to me that inflation will keep accelerating rather than decelerating over the coming months, as the rising commodity prices start to trickle down from producer prices to consumer prices more broadly.

I would also like to point out the poor performance of Norwegian krone (NOK), Swedish krona (SEK), Australian dollar (AUD), Canadian dollar (CAD) and Japanese yen (JPY) over the past 12 months, as seen from the currency market table. Not surprisingly, there are reports suggesting all-time high demand for gold in these countries and, looking 12 months ahead, I anticipate that we will get similar reports from the eurozone and the US.

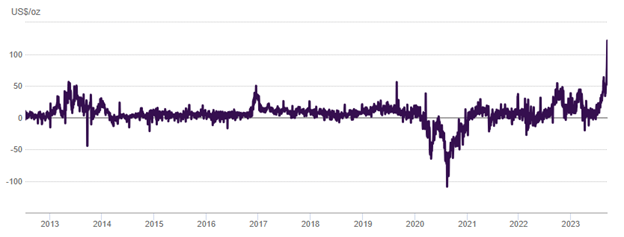

Shanghai–London gold price difference

Lately, the gold market has been buzzing about the widening difference (also known as the spread) between the price of gold in Shanghai and the price of gold in Western markets (London and New York). At a recent peak, gold was trading at a premium of more than 6% in Shanghai compared to London, which is a huge spread. To give some context, typically gold trades at a premium of less than 1.0% in Shanghai compared to London.

Shanghai gold premium to London

Premiums in Shanghai typically rise when gold prices are falling since the Chinese and Asians in general tend to buy gold when the price of gold falls. Asian investors view lower gold prices as an opportunity to buy gold at a discount and so their local buying pressure causes the spread to rise. This mindset is very different compared Western investors, who typically chase rising asset prices, especially at new all-time highs.

Asian investors on the other hand are typically sellers at all-time highs. This also can be seen from the chart above, as during the COVID pandemic there was an equally great discount for gold in Shanghai as the Chinese were selling gold coupled with severe COVID lockdowns in China, which also restricted demand. This dynamic has been described in detail in one of our articles titled The West-East ebb and flood of gold.

This time, the widening of the spread has been caused by import restrictions imposed by China during the summer. This is nothing new, as China, India, Turkey and other developing nations use import restrictions for gold to support their own currencies from time to time. Import restrictions restrict the availability of gold, which causes the local gold prices to rise, and, as I just described, Asians buy when prices are low rather than high. This in turn, ideally from the government's perspective, causes the local demand for gold to fall and the demand for their local currencies to rise. The Chinese yuan has been under pressure this year, falling close to 9% from January 2023 highs relative to the US dollar, and so the Chinese government wanted to prop up the yuan and imposed import restrictions for gold.

What is new is that the spread hit an all-time high (as far as data goes) and, as we know, all time is a long time. However, there is a lot of misinformation floating around the topic, suggesting that this is an indication that the gold markets in London and New York would be losing control over gold pricing.

Although there are differences in the market mechanics of these markets, the fact is that average trading volumes for the different markets in August were as follows: London 77.9 billion USD, New York 29.9 billion USD and Shanghai (including futures and physical gold) 16.5 billion USD. The volumes in the West are still dominant, and so the Western markets still show the way by and large for the price of gold.

As of 19 September, China seems to be lifting some of the import restrictions, and the spread has come down from the highs significantly. For the traders able to access the Chinese gold market, this has been a huge arbitrage opportunity, and arbitraging should bring the price of gold in Shanghai back in line with London and New York rather quickly. This is how things stand today, and I will continue to update this story in the Voima Markets newsletters over the coming months.

Disclaimer

The views expressed on this post are those of the author and do not necessarily reflect the official views or position of Voima.

You are allowed to copy our content, in whole or in part, provided that you give Voima proper credit and include the appropriate URL. The name Voima and a link to the original post must be included in your introduction. All other rights are reserved. Voima reserves the right to withdraw the permission to copy content for any or all websites at any time.

Nothing written in Voima's blog or website constitutes investment, legal, tax or other advice. It should not be used as the basis for any investment decision which a reader thereof may be considering. The purpose of Voima's blog is to provide insightful and educational commentary and is not intended to constitute an offer, solicitation or invitation for investing in or trading gold.