Gold in crises part 4: war

Lasse Lindholm

Community Manager

Table of contents

Introduction

The previous articles dealt with crises that were ultimately caused by bad monetary policies. The root cause for the German hyperinflation was the lackadaisical monetary policy, which caused the decoupling from the gold standard and the supply of the floating currency to be increased so much that, at the end of the day, people had to carry their money around in wheelbarrows. The root causes of the Great Depression were the Fed's bad monetary policies mixed with an overflow of borrowed capital in the stock market, and the central bank's internal dispute about the extent the banking sector should be aided in the crisis. During the Great Inflation and stagflation of 1965–1982, the main reasons had to do with the central bank neglecting its most important duty: keeping the inflation in check.

This article is about war on a general level, and how it can affect asset classes.

The root cause for the World Wars was the restructuring of the balance of power between competing nations. In his book titled “Principles for Dealing with the Changing World Order: Why Nations Succeed and Fail” Ray Dalio writes about great powers and how they seem to rise and fall in cycles historically; Dalio also writes how great powers have had to fight for their position against emerging competitors. From history, we can also see how bigger escalations between great powers often have to do with sovereignty or the threat of losing it in connection with, for example, culture, religion or areas.

War is about a demonstration of power, and warring countries eventually find themselves in a position where they can no longer retreat without losing their position of power. A war fought with armies is often the last resort for a nation, since a possible defeat or a retreat often comes with huge sanctions, not to mention the loss of power and influence. Wars often tend to escalate worse than planned, and it is a great risk in warfare that it escalates beyond the borders of the belligerents, drawing other parties into the fray.1

In order to reach the status of a great power, a nation must be able to demonstrate their power simultaneously in several areas, such as in economy, technology, geopolitics, capital and currency—and of course arms. If a nation is not strong enough to win or cannot maintain their power, it must turn to stronger partners to seek support for the above-mentioned areas.

The victor is not necessarily the one who has the strongest or biggest army but rather it is often the one who has endured the pains of warfare and who has managed to adapt to the demands of war for the longest.

With physical war comes a completely different environment into which the combatants must acclimatise themselves and in which the rules of war apply. This also signals a transition to wartime economy, in which a nation has greater legal resources to control the economy.

The economies of the greatest nations were controlled and supervised by means of wartime regulations. These regulations pertained to, among other things, the rationing of goods2, controlling of production3, price and pay controls4, import and export restrictions5 and the nationalisation of central banks6. When it comes to assets and markets, for example during WW2 the following domains were regulated, among others: stock market opening hours7, commodity prices8 9, restrictions of assets8, currency restrictions8, increase of taxation10 11, restriction of issuance and company profits12.

During the World Wars, the currencies of the antagonists were generally not accepted, since the value thereof could not be relied on. This means that gold and silver and barter were used as means and modes of exchange.13

Asset classes during war

Stocks

During the World Wars, a common measure was to close down stock exchanges, for example in the UK, Germany and Japan, which meant that investors could not rely on having access to their capital.14 Stock trading is effectively impossible, if the exchange has been closed down; the only way to trade them in such a situation would be to resort to external brokerage companies, provided that there is sufficient liquidity.

The pricing of goods and the issuance of capital is restricted more strictly during wartime, so it is difficult to assess the real value of commodities, raw materials or securities. This also affects the valuation of stocks, since the value of a company's shares is based on the value of the company itself.

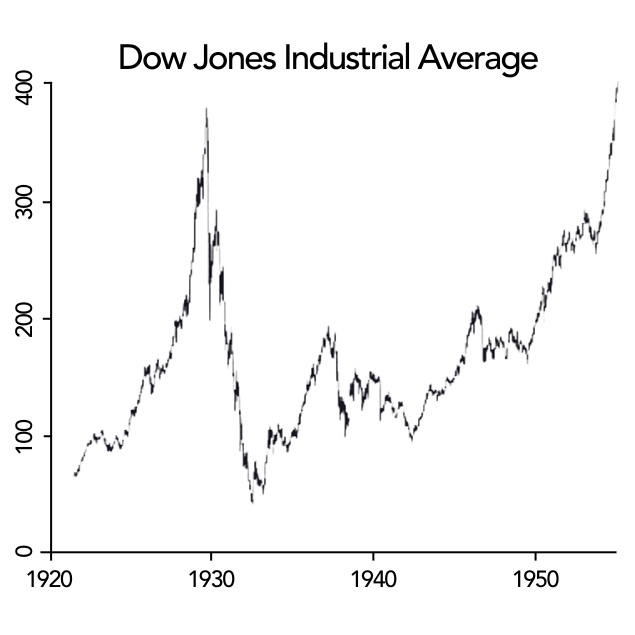

Losing the war generally means that the nation and its citizens are completely bereft of their possessions and power. During the World Wars, the value of the (still open) stock markets depended on how well the nation fared in battle. When a battle was won, the stocks went up, and when a battle was lost, the stocks went down, as shown in the graph below.

Stock exchanges are generally closed due to a lack of liquidity, since hardly anyone is willing to buy companies situated in the theatre of war. After an exchange is closed down, the value of money applies only in print, meaning that it is no longer accessible from an account or otherwise.

Bonds

When a nation loses the war, it might not be able to repay its debts or reparations, or take care of its monetary system. Like in the case of other catastrophes befalling the nation, such as natural disasters, a war-broiled country may become insolvent. The markets will take this into account very quickly.

If there is no hope of repayment, the markets will react immediately by dropping the value of bonds to zero.

In widespread conflicts, all parties typically incur debts either towards each other or to external nations and investors. It is also typical that war reparations are not fully repaid or that the repayment periods are extremely long, which enables inflation to eat away at the value of the bond-holder's capital almost completely. For example, the UK made the last repayment for its debts incurred during WW1 only in the 2010s—roughly 100 years after the war15. Out of all the countries who engaged in WW2, Finland is so far the only country who has paid its war reparations in full.

The events of war have an effect on bonds, since these can cause investors to believe that the nation in question might possibly neglect to pay back its debts or otherwise affect the repayment period. Thus the circumstances affecting the interest rates of the securities of all nations should also affect the bond prices.

The nation can also finance its war by raising it from its own citizens or from foreign partners in the form of war bonds.

All in all, bonds are not a safe investment during war, since the solvency of the nation who offers them is anything but guaranteed.

Housing

In war, houses are destroyed and areas can be conquered, which has a severe impact on the state of the housing market. People have to move away from their homes and seek new places elsewhere away from the conflict areas. Generally, the economy of a nation can be long in tumult after the war and it may take a long while before the housing market begins to flourish again.

In the short term, war destroys property and real estate, depriving people of the latter as areas are invaded. The value of the property adjacent to the theatre of war decreases swiftly if the war expands to new territories, which causes the people living in the vicinity to move further away, thus rendering their houses worthless. Often the only potential (and able) buyers of the real estate in the areas of conflict are the banks, and the purchases are often done way below the normal prices. The real estate and housing situated farther away from the conflict areas often retain their prices better due to rising demand.

Houses and apartments in the war zone thus lose their value, possibly completely, and those areas that are not destroyed or that have been bought by banks, could be a source of manifold profit for banks. Wars affect also outside the conflict areas, since often the conflict escalates beyond the boundaries of a particular country.

The graph below shows how the US housing market reacted to the two World Wars. After WW2 in 1945, the price of housing started to go up, since many people returning from the war were looking for a place for their family.16 17 Back in those days, there was a great dearth of housing, and the returned soldiers had to find temporary lodgings and wait to get a bigger house or apartment. The need for houses was further increased by the post-WW2 baby boom.

Gold

The best items to retain their value during war are often energy, oil, consumer products, arms and security items, to name a few. Compared to these, gold is not as essential when it comes to warfare, but nonetheless gold has a wholly unique role during war which makes it worthwhile to own some. Gold is liquid, it is universally recognised and it is easy to transfer from one place to another. These three characteristics can be even more important or valuable than gold's potential exchange rate with paper money in the midst of the crisis. And one must not forget perhaps the most important characteristic of gold, its ability to store value—something that happens also during war.

The price of gold can go up or down in relation to paper money, but gold has always returned to its position as a store of purchasing power when compared with other commodities or means of exchange. Gold has been and still is a store of value in circumstances when the economy and society are in disequilibrium and asset classes have crashed in value. Gold has thus always worked as a safe haven, as has been shown in the previous parts of this article series. Gold's role has remained similar through the darkest decades of history, like in the 1910s and 1940s, among other periods.

This safe haven attracts investors especially when geopolitical tensions are growing heated. This happened during the Gulf War in the 1990s, the 9/11 attacks in 2001, the Iraq invasion in 2003, in 2014 when the US went to Syria and most recently when Russia invaded Ukraine in 2022. War or even the threat thereof is valuated immediately in the markets, and it shows in the value of the affected nation immediately.

Naturally, there is always the possibility that a nation will confiscate the gold ownings of its citizens, like the Axis powers did during WW2. However, it is a whole different matter, how this is supposed to be carried out in practice.

Furthermore, the financing of war increases money printing and accelerates the growth of national expenses. In such a scenario, gold's safe haven status is particularly apt.

Summary

As a nation becomes a party to a war, in one way or another, it often enacts wartime regulations which regulate the nation's revenue and production and the ownings of its citizens, among other things. When one also takes into account the destructive reality of war, one is left with a very uncertain period of time in the history of that nation—especially, if that nation is the underdog.

In war, various asset classes are often on the knife's edge. For example, as happened in the World Wars, nations can close down stock exchanges due to a lack of liquidity, making stock trading virtually impossible. Furthermore, the activities of companies are restricted for example when it comes to raw materials or production, which is naturally reflected in the value of the company's shares. Bonds are directly connected with the solvency of the issuing nations, and this solvency is doubtful during wartime—especially, if the nation is not faring well in battle. And the ugly reality with housing is that bombings and other offensives can cause considerable damage to investments.

With gold, the situation is different. Gold is not connected to the event of a single nation, and thus its value is not directly related to any single nation's success in war. Because gold cannot be created out of thin air, there is no fear that any country could bring down the value of gold by increasing its supply overmuch. Thus, gold remains a safe haven even in the midst of war.

The views expressed on this post are those of the author and do not necessarily reflect the official views or position of Voima.

You are allowed to copy our content, in whole or in part, provided that you give Voima proper credit and include the appropriate URL. The name Voima and a link to the original post must be included in your introduction. All other rights are reserved. Voima reserves the right to withdraw the permission to copy content for any or all websites at any time.

Nothing written in Voima's blog or website constitutes investment, legal, tax or other advice. It should not be used as the basis for any investment decision which a reader thereof may be considering. The purpose of Voima's blog is to provide insightful and educational commentary and is not intended to constitute an offer, solicitation or invitation for investing in or trading gold.

-

https://odessa-journal.com/nato-rules-out-the-normalization-of-relations-with-russia-after-the-end-of-the-war-in-ukraine/ ↩

-

https://yle.fi/aihe/kategoria/elava-arkisto/pula-ajan-saannostelya-ja-korvikkeita ↩

-

https://www.defense.gov/News/Feature-Stories/story/Article/2128446/during-wwii-industries-transitioned-from-peacetime-to-wartime-production/ ↩

-

https://www.encyclopedia.com/social-sciences-and-law/economics-business-and-labor/economics-terms-and-concepts/wage-and-price-controls#:~:text=Wage%20and%20price%20controls%20were,inflation%20fighter%20and%20food%20rationer. ↩

-

https://blogs.worldbank.org/voices/trade-restrictions-are-inflaming-worst-food-crisis-decade ↩

-

https://www.federalreservehistory.org/essays/feds-role-during-wwii ↩

-

https://www.investmentoffice.com/Observations/Markets_in_History/August_1914_When_Global_Stock_Markets_Closed.html ↩

-

https://www.finlex.fi/fi/laki/ajantasa/2011/20111552 Luku 4 ↩

-

https://www.taloudenperusteet.com/kirjoja/hazlitt/2-osa/17-luku-valtiollinen-hintojen-kiinnittaminen/ ↩

-

https://www.vero.fi/globalassets/tietoa-verohallinnosta/esitys--ja-opetusmateriaalit/381v09_verotuksen_historiaa.pdf ↩

-

https://www.history.com/this-day-in-history/war-revenue-act-passed-in-u-s ↩

-

https://library.cqpress.com/cqresearcher/document.php?id=cqresrre1942110600 ↩

-

https://encyclopedia.1914-1918-online.net/article/war_finance ↩

-

https://www.investmentoffice.com/Observations/Markets_in_History/August_1914_When_Global_Stock_Markets_Closed.html ↩

-

https://www.cnbc.com/2015/03/09/uk-finally-finishes-paying-for-world-war-i.html ↩

-

https://observationsandnotes.blogspot.com/2011/07/housing-prices-inflation-since-1900.html ↩

-

https://www.encyclopedia.com/education/news-and-education-magazines/housing-1929-1941 ↩

Copyright © 2026 Voima Gold Ltd. Business ID: 2843889-9. Terms of service and privacy policy. 🍪 This website uses cookies. Read more about Voima's tracking practices.